How do Australians manage their money? Where do they turn to for financial advice? And how do they budget for a rainy day? As the cost of living rises, these questions about Australian financial behaviours are more important than ever. To find the answers, Employment Hero partnered with YouGov to survey 1,500+ Australians who are working or looking for work.

The goal: to discover how the average Aussie manages their money —where they get advice, how they handle unexpected expenses, where they turn to when money’s tight, and much more. The results, weighted to the Australian working population, are eye-opening.

What you need to know

Don’t have time to read the full report? Here are our top 6 takeaways:

3 in 4 Aussies have trouble budgeting

The majority (73%) of Australians have difficulty budgeting, with 3 in 4 saying it’s hard to budget for a whole month as they don’t always know what expenses might arise. Families with children under 18 at home, and Gen Z are the most likely to struggle to stick to their monthly budgets.

Unexpected expenses hit the wallet hard

Almost 1 in 10 (9%), or approximately 1.1 million Australians, are struggling to make ends meet as the cost of living rises. And 23% of Australians —about 2.8 million — admit that they make just enough money to cover their regular expenses, and would struggle if unexpected expenses came up.

90% of Aussies have outstanding short-term debt

A staggering 90% of Australians have outstanding short-term credit debt, amounting to almost $38 million owing in debt Australia-wide. The average amount of debt per person is $4,331.

Late financial payments lead to long-term headaches

More than half (51%) of Australia has missed or been late on a financial payment, which can result in significant additional fees and charges. It’s concerning that of this group, 37% (or 2 in 5 people) miss or are late on financial payments at least once per year.

Money stress takes its toll

Stressing over finances can cause serious damage to Australian lives, with over 7 in 10 (72%) experiencing negative emotions or behaviours —like a lack of motivation, losing sleep, and binge habits —as a result of their financial situation.

Cost of living pressures rise

Almost 1 in 2 (46%) of Australians struggle to pay for regular expenses like rent and food before payday. 18% say this happens often, and 28% say that they are sometimes unable to pay for expenses like rent, food and transport before their regular paycheck.

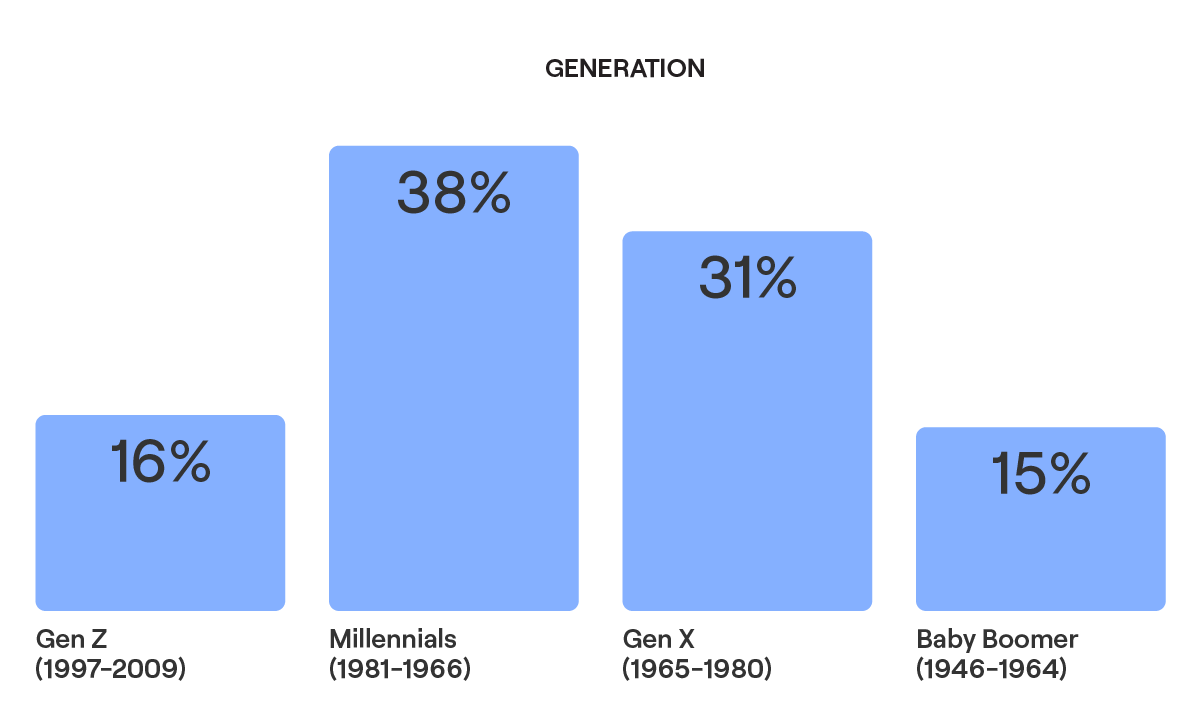

Who did we survey?

We surveyed 1,500+ members of the YouGov Plc Australian panel who were currently working or actively looking for work. The research results have been weighted using the latest Census data to the profile of working Australians, making the research results statistically representative of the overall working population.

Let’s dig into the detail

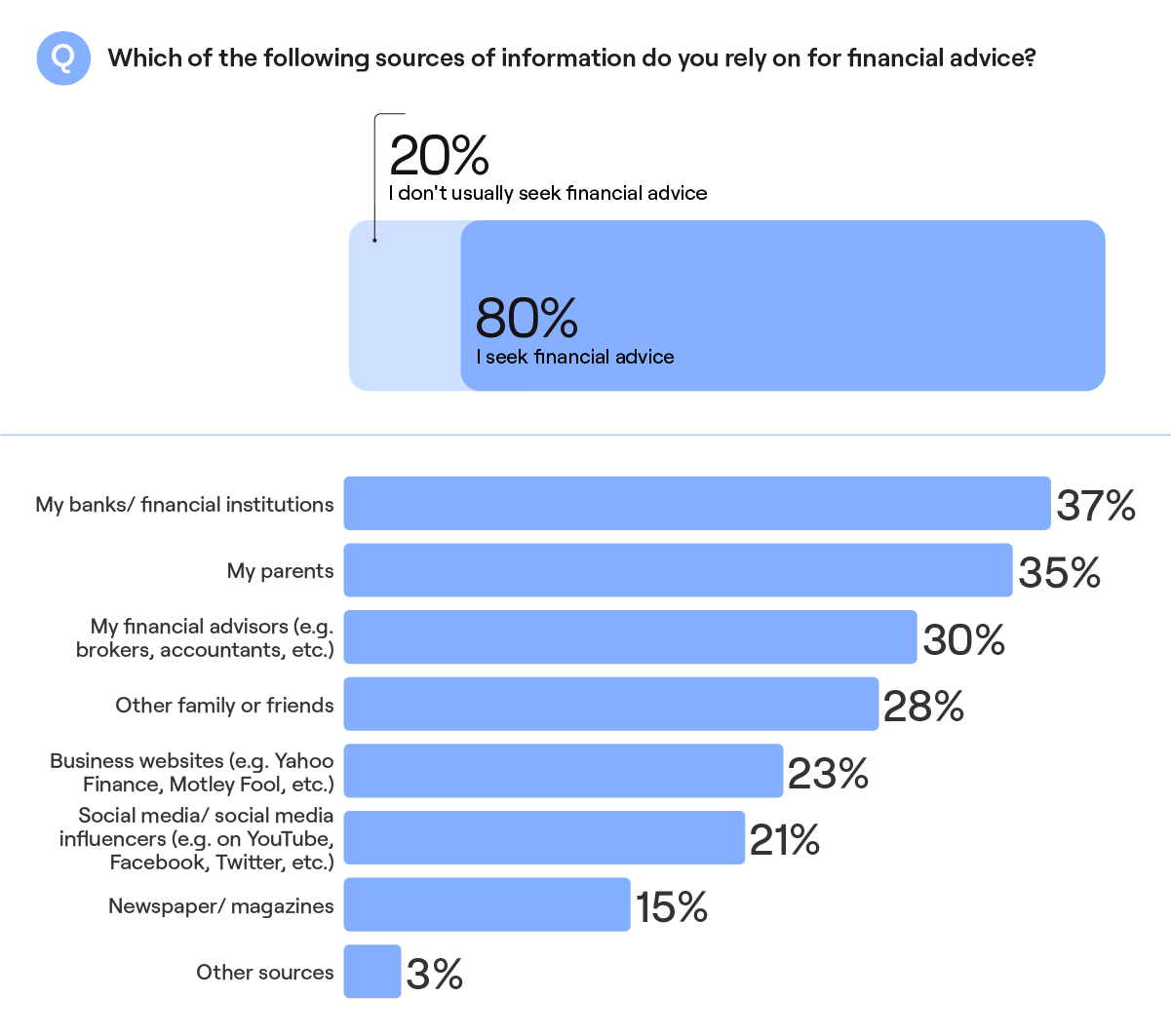

Banks, books or mum and dad: Who do we turn to for financial advice?

Key Insight: People looking for financial advice will turn most often to their banks (37%) and their parents (35%) for guidance, with younger generations more likely to seek financial advice than their older counterparts (Gen Z 85%, Millennials 88% compared to Gen X 75% and Baby Boomers 66%). These younger generations turn to social media influencers as a main source of financial advice.

Gen Z looks to social media

1 in 4 Gen Z members (24%) say they rely on social media and social media influencers for financial advice.

Younger generations are more likely than their older counterparts to say that they rely on their parents for financial advice. 61% of Gen Z look to their parents for advice, compared to just 27% of Gen X.

85% of Gen Z seek financial advice, compared to only 66% of Baby Boomers.

Millennials turn to influencers (and the ‘Bank of Mum and Dad’)

Nearly 1 in 3 Millennials (30%) say they rely on social media influencers for financial advice

Millennials are the most likely to seek financial advice (88%) and 43% turn to their parents for financial advice

Gen X don’t want advice from their parents75% of Gen X seek financial advice, but only 27% rely on their parents for financial advice, a much lower percentage than Gen Z and Millennials.

Baby Boomers least likely to seek any advice:This generation is the least likely to seek financial advice from any source. Only 66% of Baby Boomers seek financial advice.

Lower income households less likely to seek advice Lower income households are less likely to seek financial advice, with 70% of households under $50K seeking advice, compared to 89% of households with incomes of $150K+

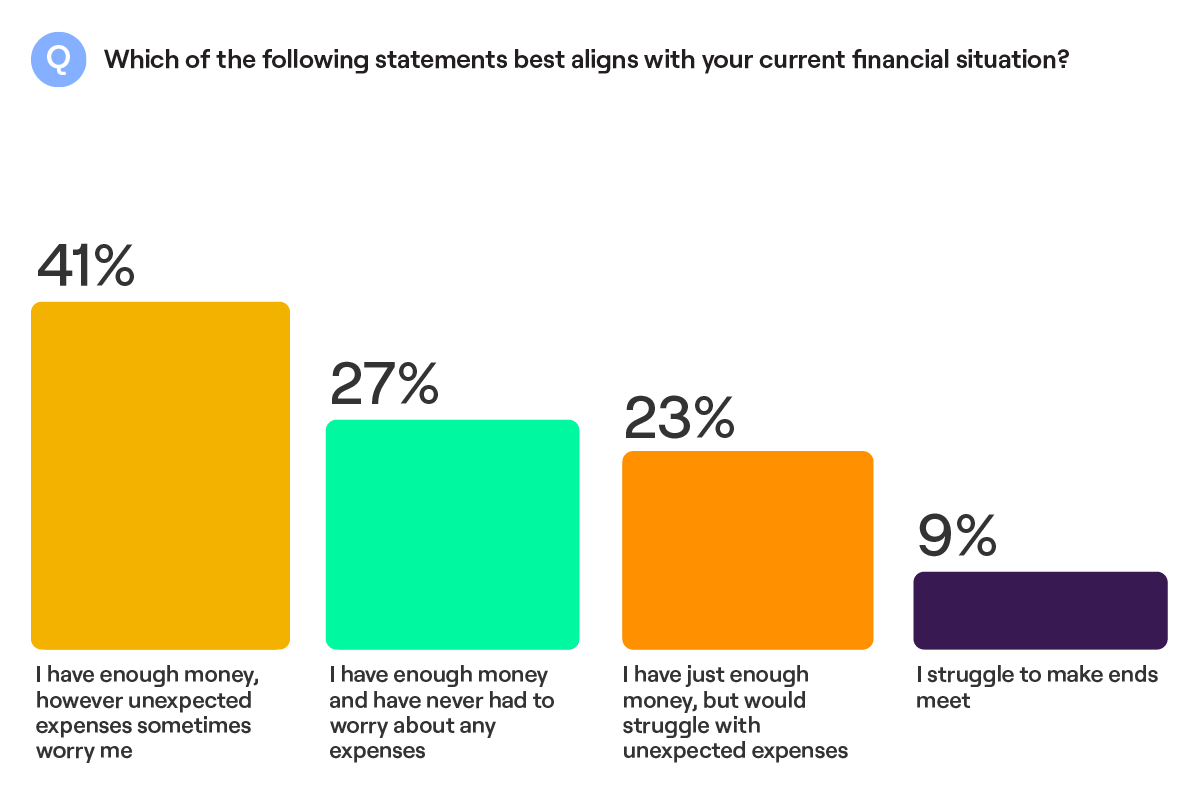

Millions of Australians struggling to make ends meet

Key Insight: Millions of Australians are struggling to make ends meet and handle unexpected expenses. Close to 1 in 10 (9%), or approximately 1.1 million Australians who are working or looking for work, are struggling to make ends meet. And 23% of Australians —about 2.8 Million — admit that they make just enough money to cover their regular expected expenses, and would struggle if unexpected expenses come up.

For a sizable proportion of Australians (41%), even though generally they have or make enough money to support themselves/ their family, unexpected expenses can still sometimes worry them.

Women more likely to be financially disadvantaged:

Women are 36% more likely than men to be in a disadvantaged financial situation. Over 1 in 10 (11%) women say that they struggle to make ends meet compared to 7% of men.

Baby boomers struggle to make ends meet:

1 in 7 (14%) baby boomers say that they struggle to make ends meet, which is twice as likely as the young generations (Gen Z 6% and Millennials 7%).

Tip: Work app has a bunch of feature that can help you lower the cost of living by providing increased purchasing power for everyday essentials. Benefits, through Employment Hero’s vast network of 200,000+ SME customers and 1M+ global employees, negotiates significant discounts from popular retailers like Big W, Uber Eats, Caltex, and others.

We work with employers to offer these benefits to Work app users, to help them maximise their pay and alleviate the financial strain caused by soaring grocery, fuel, and rent prices. Learn more here.

Less than half of millennials make enough to support themselves and their family

49% of Millennials say that they generally make or have enough money to support themselves and their family, however unexpected expenses can still sometimes worry them, which is more likely than other generations.

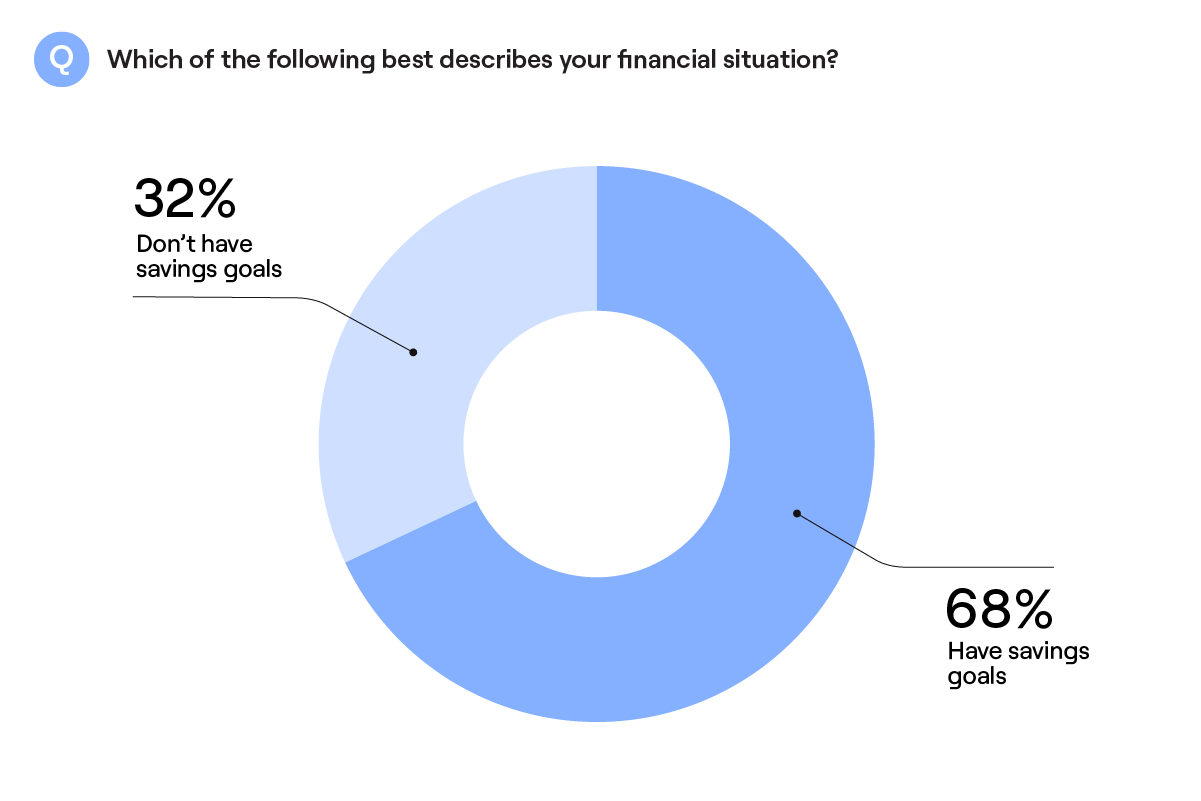

Savers vs Non-savers: Who’s struggling?

23% of people who don’t have savings goals struggle to make ends meet, compared with just 3% of people with savings goals.

Which generation are the best savers?

Key Insight: Despite their best efforts, millions of Australians are struggling to save —and it has a lot to do with what generation you’re in. While two thirds (68%) of Australians have saving goals, more than a third (37%) say they don’t always stick to their goals despite best intentions.

What’s more worrying is that 10%, the equivalent of about 1.3 Million, don’t have any emergency savings.

Millennials kick savings goals:Millennials are the generation most likely to have savings goals with almost 4 in 5 (78%) saying that they do compared to 70% Gen Z, 63% Gen X and 52% Baby Boomers.

Tip: The Work app has a range of features to help you budget and save better every day. Features like Pay Split and Stash accounts helps you allocate your income into dedicated savings for bills, emergencies, groceries, and more.

Upcoming products like Bill Management provide discounts on essential bills so you can save more on your regular electricity and gas costs. If you work for an organisation that uses Employment Hero, these bills can be automatically deducted from your payslip.

No savings goals for half of Baby Boomers

This is the generation most likely to not have savings goals. A sizeable 48% of Baby Boomers say they don’t set savings goals. Compare this to millennials, where only 22% say they don’t have savings goals.

Queenslanders shun savings:Queenslanders are almost twice as likely as those living in NSW and SA to admit that they don’t have any emergency savings nor savings goals. 16% of QLDers say they don’t have any emergency savings nor savings goals, compared to 8% of those from NSW 8% and 9% of those from SA.

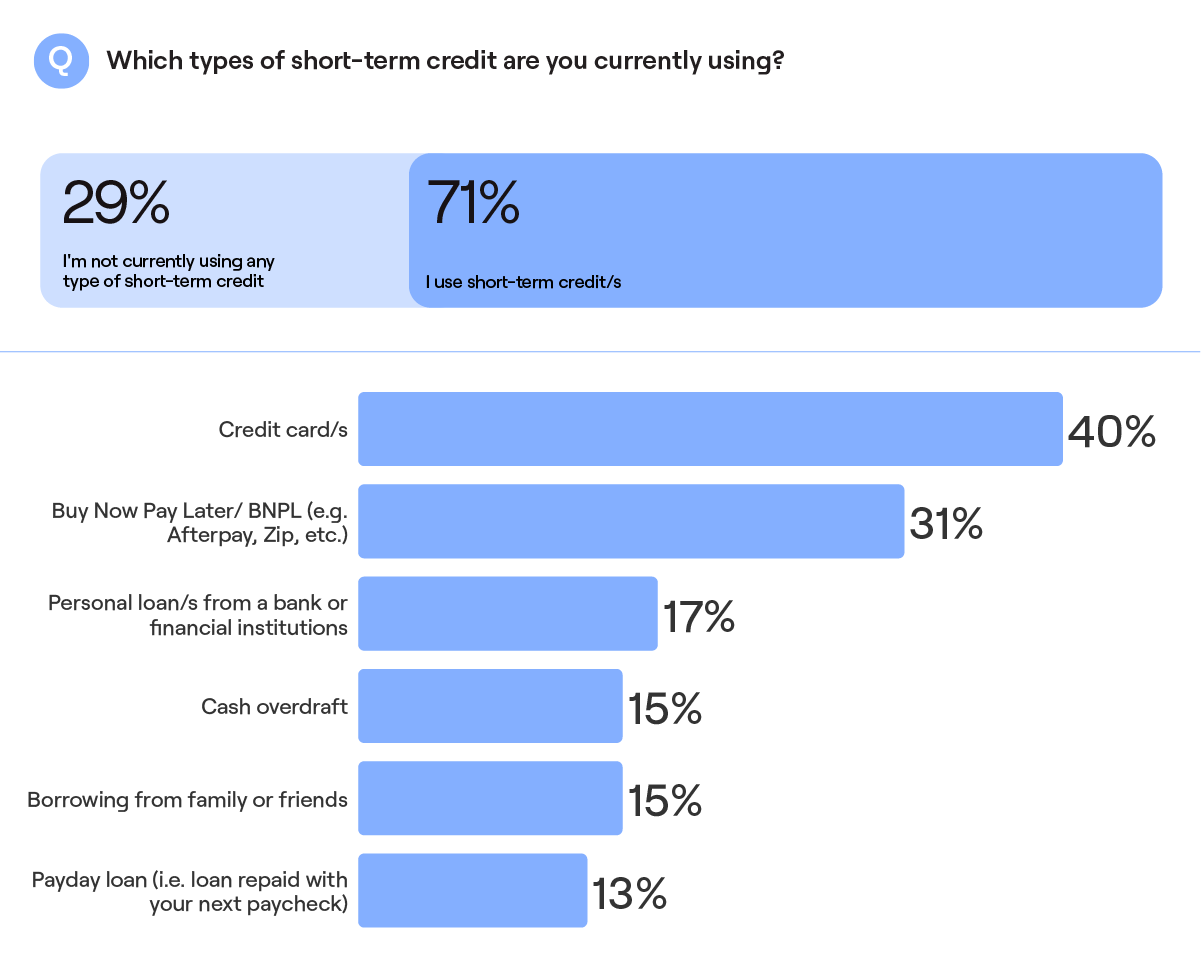

Short-term credit fuels our lives

Key Insights: The majority of Australians are using short-term credit to fund their lives. Among Australian workers and those looking for work, over 7 in 10 (71%) are currently using short-term credit to fund their lives, with the most common forms of credit being credit cards (40%) and Buy Now Pay Later (31%).

Millennials most likely to lean on short-term credit

Millennials and Gen X are more likely than Gen Z and Baby Boomers to be using short-term credit (Millennials 78%, Gen X 73% compared to Gen Z 59% and Baby Boomers 58%).

Millennials are the generation most likely to be using BNPL (38%) and payday loans (18%).

Did you know:Short-term debt is defined as debt obligations that are due to be paid within one year. While $4,331 may not seem like a large sum, short-term debt often comes with high interest rates. To help users avoid high-cost, high-interest credit options, Work app provides employees of Employment Hero organisations with Earned Wage Access (EWA) tools. Earned Wage Access helps users avoid costly, short-term credit options like Buy Now Pay Later, credit cards and payday loans. To learn more about Earned Wage Access, head here.

Full time vs Part time

Full time workers are more likely to be using short-term credit, with 77% or over 3 in 4 using short-term credit. In comparison, only 63% of part-time workers use short-term credit, and 58% of those looking for work use short-term credit.

Short-term credit bridges the payday gap

Out of those who are often or sometimes unable to pay for regular expenses before payday, 84% use short-term credit to bridge the payday gap.

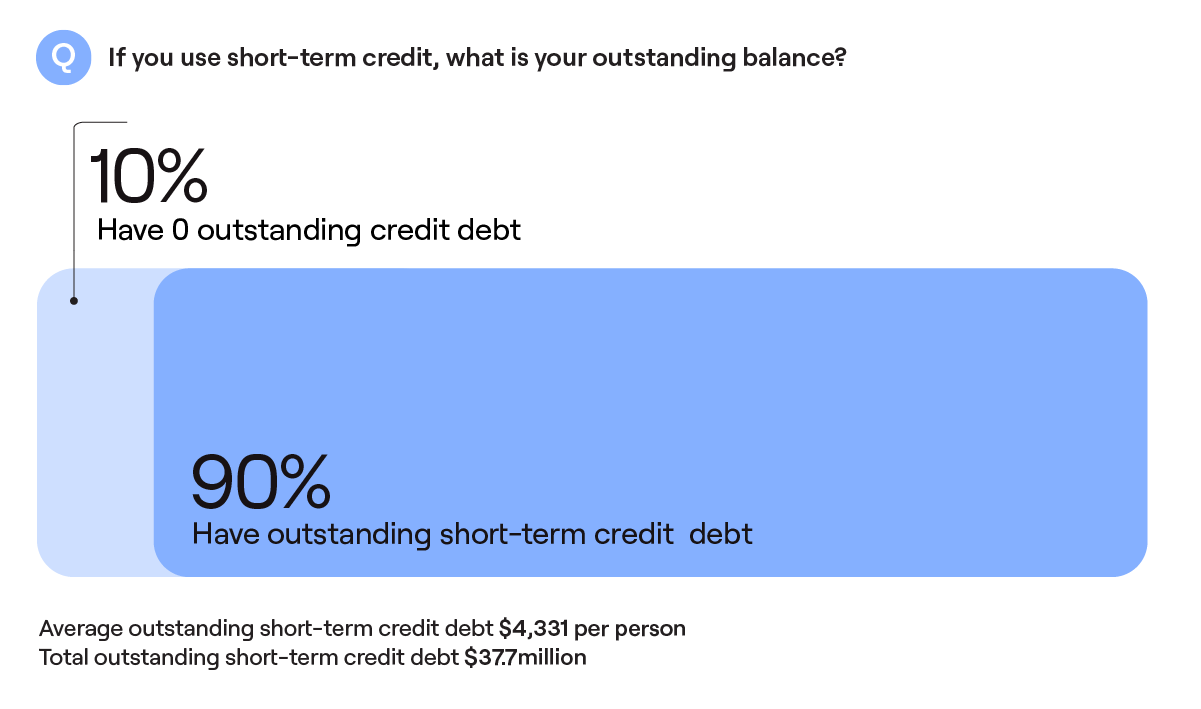

90% of Aussies have outstanding short-term debt

Key Insights: A staggering 90% of Australians surveyed who are working or looking for work have outstanding short-term credit debt. The average amount of debt per person is $4,331, which could potentially amount to almost $38 million owing in debt Australia-wide.

Short-term debt is defined as debt obligations that are due to be paid within one year.¹ While $4,331 may not seem like a large sum, short-term debt like credit and payday loans often comes with high interest rates. Using the Australian Government’s MoneySmart credit calculator,² we can see that if you had $4,331 in outstanding credit card debt, at an average interest rate of 18%, and you were only making minimum repayments each month, you’d end up paying $14,619 over the course of the loan. It would take you 30 years and 9 months to pay off this debt —and you would have paid $10,288 in interest³.

How much debt does the average Australian have?

Over 1 in 10 (11%), the equivalent of 988,000 Australians, have a total short-term credit outstanding balance of more than $10,000

Nearly 1 in 5 (18%) have an outstanding short-term credit balance greater than $8,000.

Men have higher average debt and are more likely to miss financial payments.

On average, men have higher levels of debt than women. Men have an average of $4,901 of short-term debt, while women have an average of $3,680 of short-term debt.

Men are also more likely than women to have missed or been late on a financial payment (55% compared to 46%).

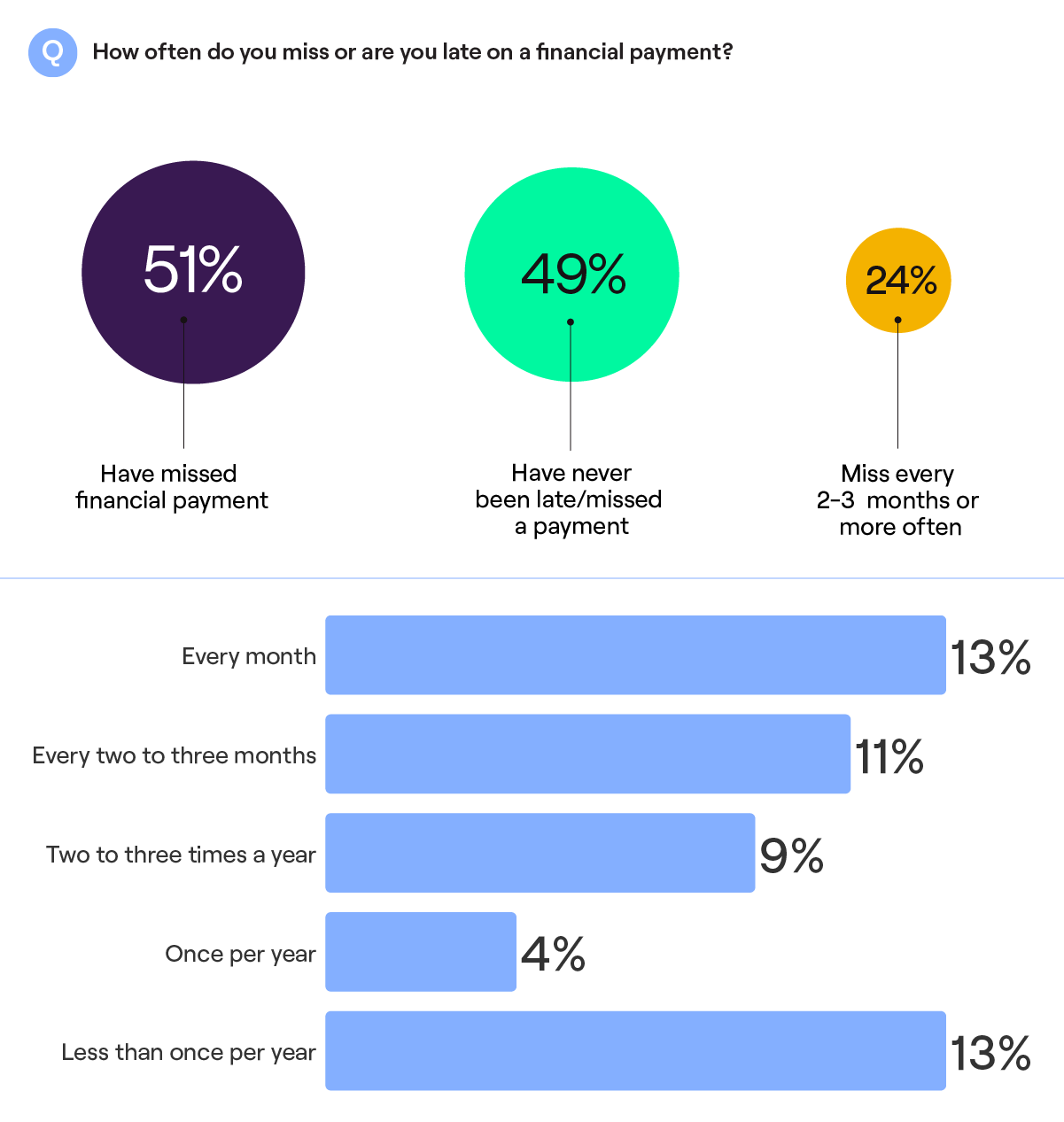

Up to 1.6M Aussies miss financial payments every month

Key Insight: Among Australian workers and those looking for work, more than half (51%) have missed or been late on a financial payment, which often results in additional fees and charges. And a staggering 13% or up to 1.6 million Aussies miss financial payments every month.

How often do Australians miss credit repayments?

At some point: Over half (51%) of Australians who are working or looking for work have missed or been late on a financial payment.

At least once per year: Nearly 2 in 5 (37%) say that they miss or are late on their financial payment(s) at least once per year.

At least quarterly: 1 in 4 (24%) say that they miss or are late on their financial payments every 2-3 months or more often.

Every month: 13% of those surveyed —that’s the equivalent of 1.6 million Australians —say that they miss or are late on their financial payments every month. This can result in significant additional fees and charges, and push people further into cycles of debt.

WA leads Australia in late financial payments

1 in 5 (20%) of Western Australians say that they miss or are late on their financial payments every month. That’s far more likely than those from other states, including NSW (12%), VIC (13%), QLD (12%) and SA (9%).

Gen X most likely to miss financial payments

Nearly 1 in 5 (18%) Gen X say that they miss/ are late on their financial payment(s) every month, which is more likely than all other generations (Gen Z 10%, Millennials 12% and Baby Boomers 7%).

Men 20% more likely than Women to miss payments

55% of Men say they have missed or been late on a financial payment, compared to 46% of women.

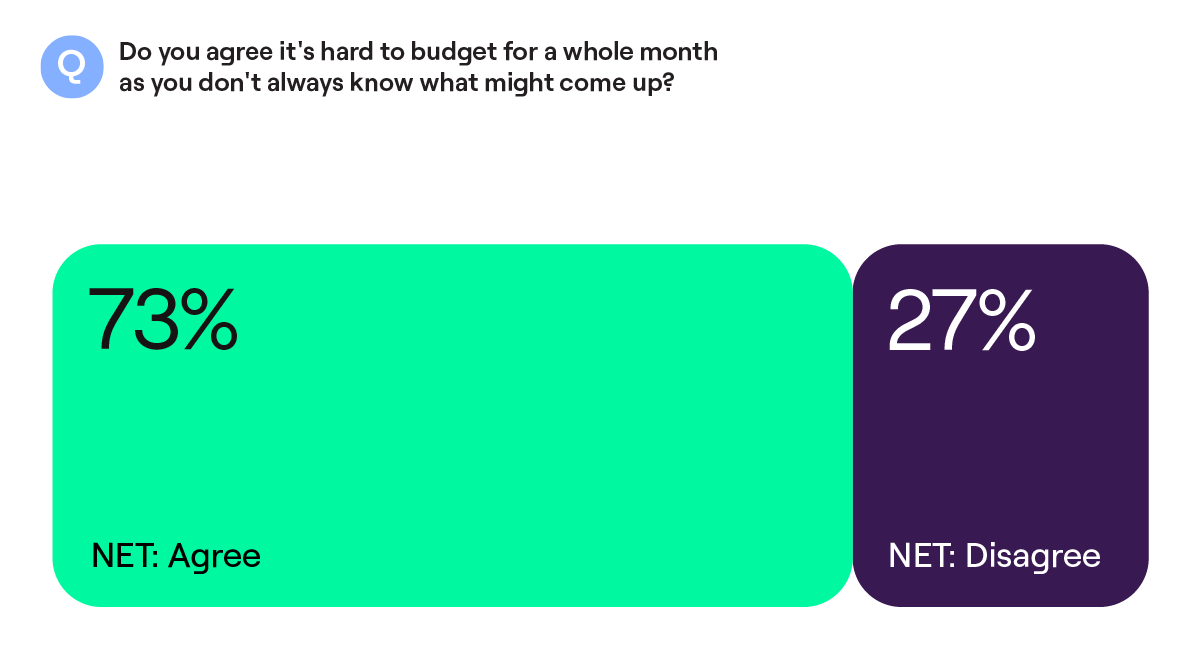

3 in 4 Aussies have trouble budgeting

Key Insights: The majority (73%) of Australians have difficulty budgeting, with 3 in 4 saying it’s hard to budget for a whole month as they don’t always know what expenses might arise. Families with children under 18 at home, and Gen Z are the most likely to struggle to stick to their monthly budgets.

Families struggling to budget

80% of those with children under 18 at home agree that it’s hard to budget for a whole month. Compare that with those who don’t have children living at home —just 67% say that it’s hard to budget for the month ahead.

Gen Z most likely to struggle

Gen Z is the most likely to agree (79%) that it’s hard to budget for a whole month, while only 59% of Baby Boomers feel the same.

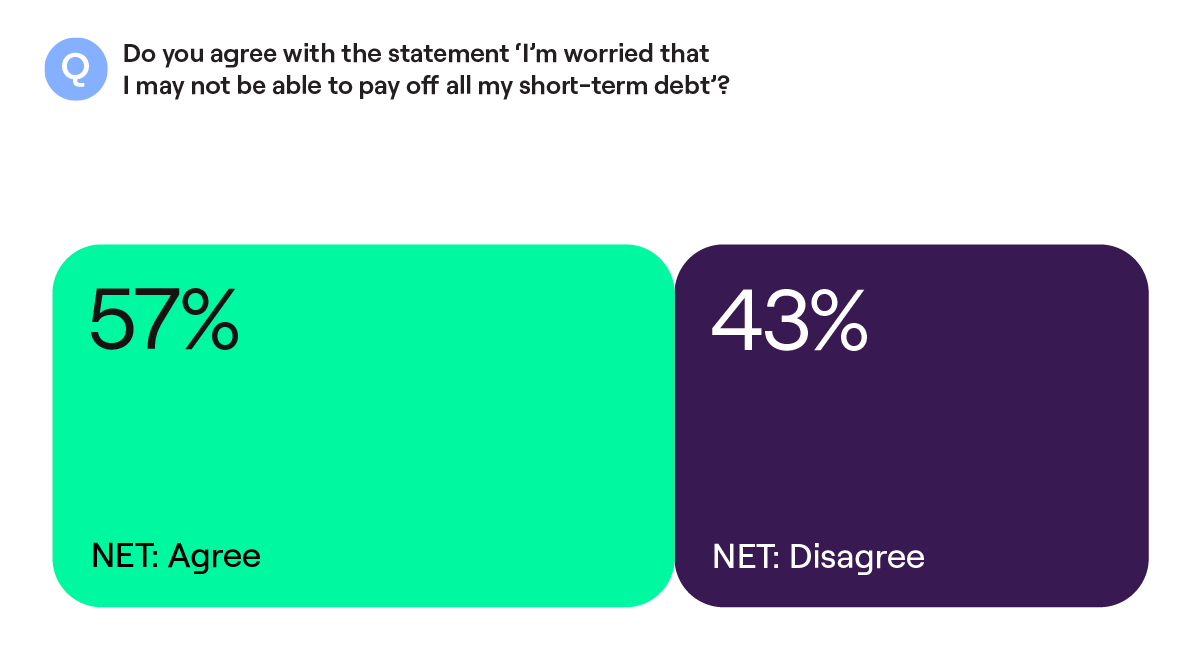

Short-term debt becomes a long-term worry

Key Insights: Short-term debt is weighing heavy on the minds of 4.5 million Australians, with nearly 3 in 5 (57%) worried they may not be able to pay off all their short-term debt. Men are more likely than women to be worried about not being able to pay off all their short-term debt (63% compared to 50%). Younger generations are the most likely to be worried about paying off their short-term debt. 58% of Millennials and 61% of Gen X are worried about this, compared to just 43% of Baby Boomers.

Tip: The average Aussie has $4,331 owing in short-term debt —and it’s causing serious worry. Short-term credit carries high interest rates —up to almost 20% interest —and can lead people into serious debt spirals.

Earned Wage Access is a Work app feature that allows employers to offer their employees a way to avoid short-term credit, loans and high-interest repayments. It provides employees with on-demand earned wage access (EWA), allowing them to access up to 50% of their earned wages before payday, capped at a maximum of $250 per week. Since it’s money an employee has already earned, there’s no credit, loan or interest involved. Learn more here.

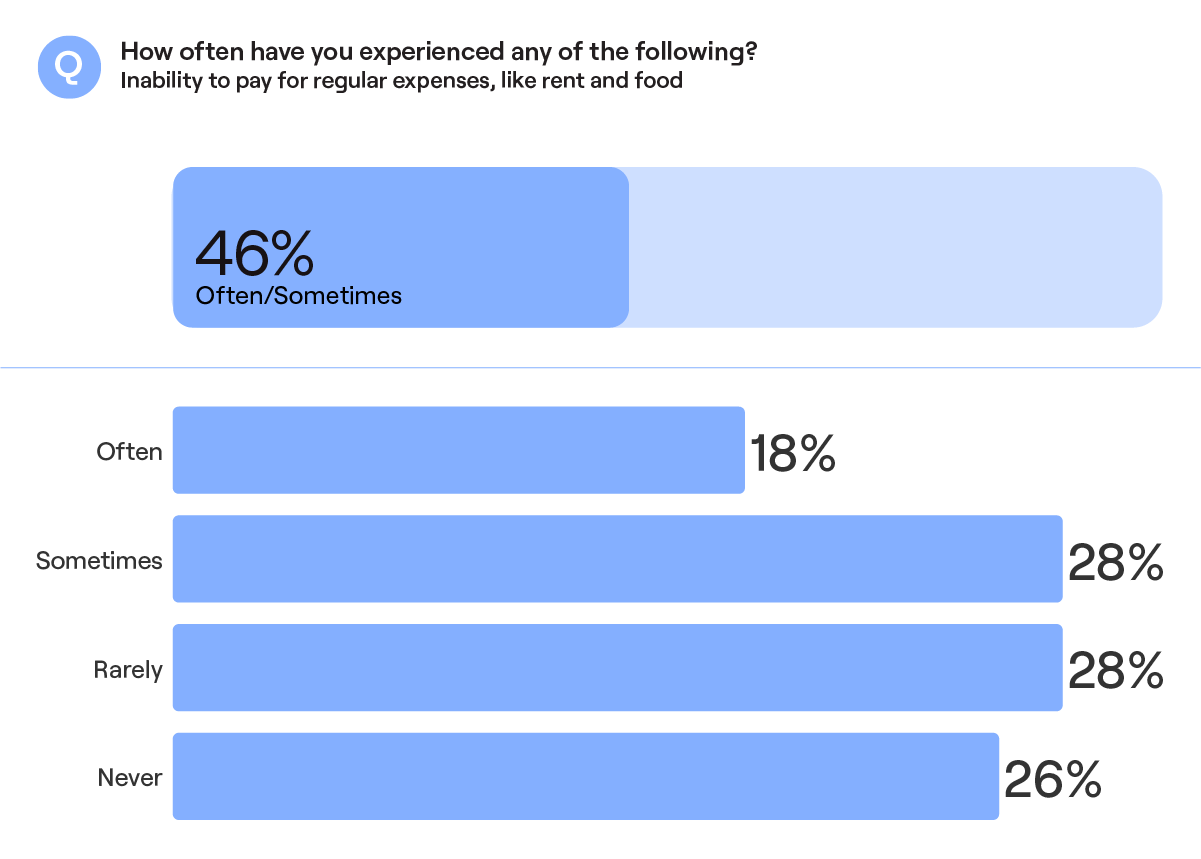

1 in 2 Aussies struggle to pay for regular expenses before payday

Key Insight: Almost 1 in 2 (46%) Australians are struggling to pay for regular expenses like food and shelter before payday. Almost half (46%) of Australians say that they are often (18%) or sometimes (28%) unable to pay for regular expenses like rent, food and transport before payday.

Families 3X more likely to run out of money before payday

Those with children under 18 at home are 3X as likely as those without to often run out of money to pay for their regular expenses before their pay day (29% compared to 10%).

Gen X struggling to pay for regular expenses

Over 1 in 4 (27%) Gen X admit that they often run out of money to pay for their regular expenses before their pay day, which is more likely than other generations (Gen Z 14%, Millennials 17% and Baby Boomers 7%).

Full time workers vs Part time: Who can pay the rent? Full-time workers are more than twice as likely as part-time workers to often run out of money to pay for their regular expenses before their pay day (22% compared to 10%).

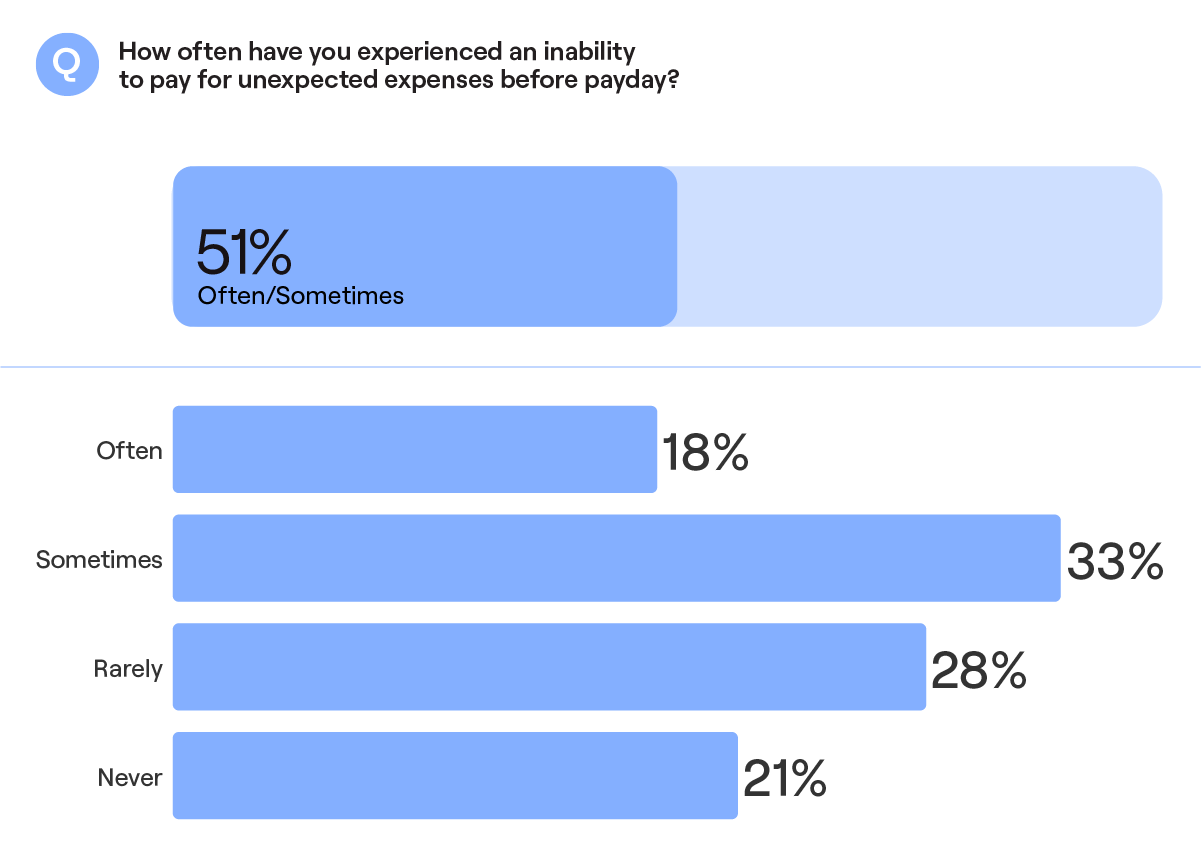

Unexpected costs leave a dent in the wallet

Key Insight: 1 in 2 Australians struggle to pay for unexpected expenses like doctor’s bills, car repairs or veterinary visits before payday. Among those surveyed, 51% say that they are often (18%) or sometimes (33%) unable to pay for an unexpected expense or emergency before their payday.

Unexpected expenses affect men more than women

Men are more likely than women to often run out of money to pay for unexpected expenses before their pay day (21% compared to 14%).

A quarter of Gen Xers often struggle with unexpected expenses

1 in 4 (25%) Gen Xers say that they often struggle to pay for unexpected expenses, which is far more likely than Millennials (14%) and Baby Boomers (12%).

Tip: Tools like Stash accounts can help you allocate your income into dedicated sub-accounts for bills, emergencies, groceries and more. Users who have set up a Spend account will be able to open up to nine sub-accounts to transfer and allocate funds from their main Spend account.

You can name these accounts, and set targets to help budget better and track expenses. Stash accounts can be set up for Travel, Bills, Groceries, Wellness, Social events and more. We designed Stash accounts to give users complete visibility of their expenses to simplify budgeting.

QLD and WA falling short most often

Those living in QLD (22%) and WA (23%) are more likely than those from VIC (14%) to say that they are often unable to pay for unexpected expenses before their pay day.

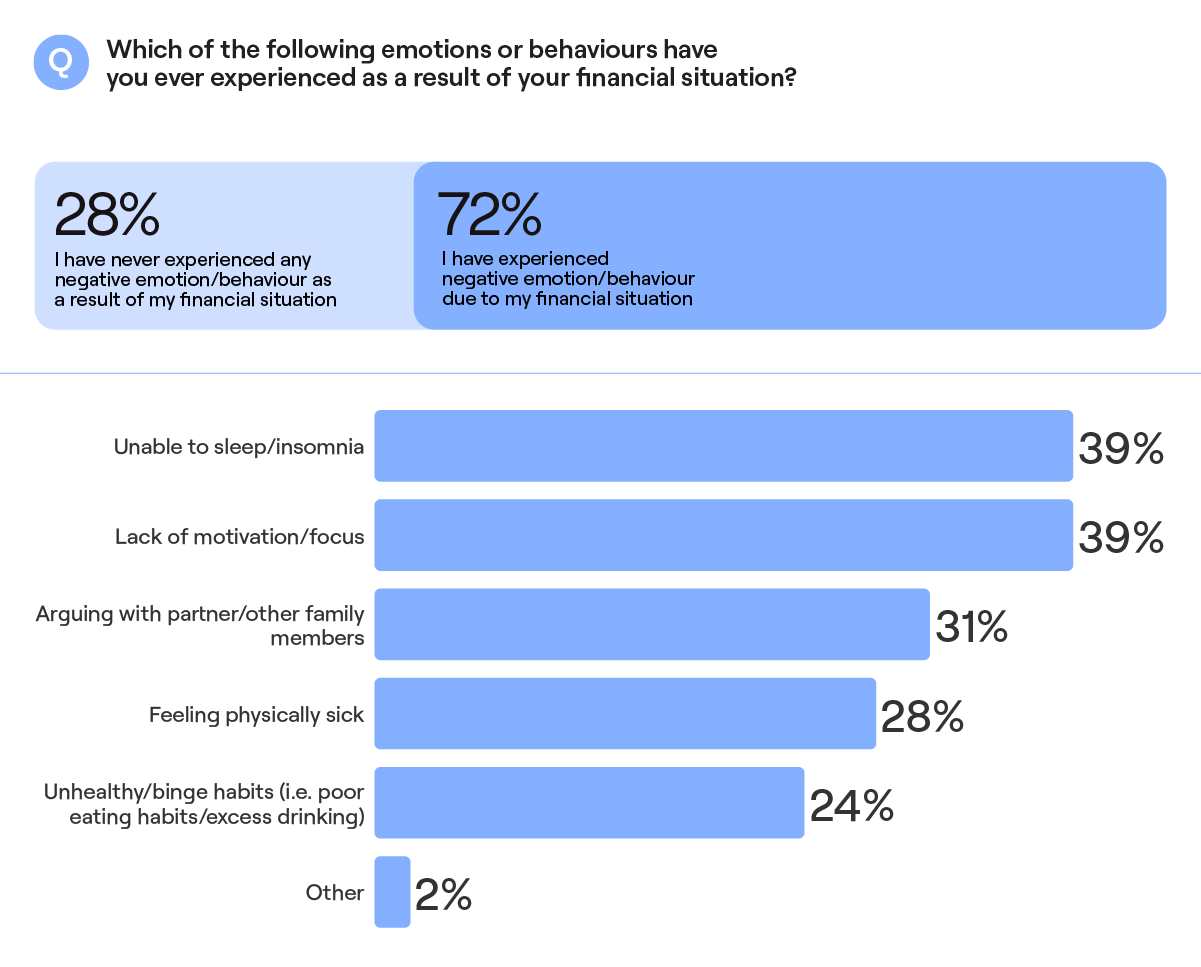

Financial stress leads to unhealthy habits

Key Insight: Over 72% of Aussies have experienced negative emotions or behaviours as a result of their financial situation.These figures tell a dark story about the impact that poor financial wellbeing has on Australian lives and families.

Losing sleep over money

2 in 5 have experienced insomnia/ felt unable to sleep (39%) due to their financial situation

Motivation takes a dive

39% of respondents have felt a lack of motivation/focus (39%) due to their financial situation.

Loved ones suffer

Financial hardship is causing rifts between loved ones, with almost 1 in 3 (31%) saying that their financial situation has previously caused them to argue with their partner/ family members.

Binge habits take control

Meanwhile, nearly 3 in 10 (28%) have previously felt physically sick and 1 in 4 (24%) have fallen into unhealthy/ binge habits (e.g. poor eating habits, excess drinking, etc.) as a result of their financial situation.

Millennials most affected

Difficult financial situations have also caused lack of motivation and focus in nearly half of Millennials (46%) compared to only 34% of Gen X and 32% of Baby Boomers.

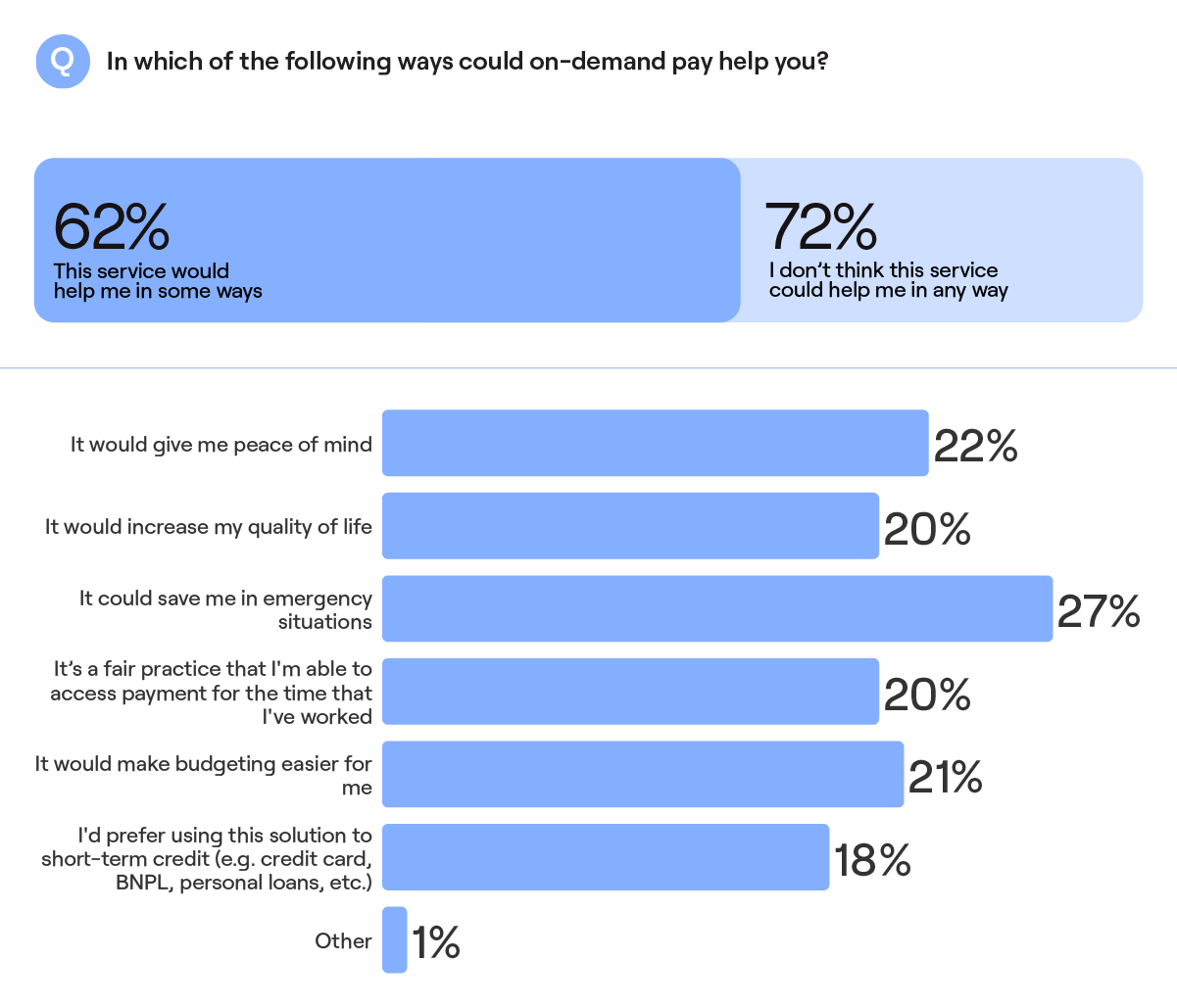

On-demand pay paves the way for financial freedom

Key Insight: The majority (62%) of Australians who are working or looking for work believe that on-demand pay/earned wage access solution could help them in some way(s). The most commonly perceived benefit is that it could save them in emergency situations (27%).

Earned Wage Access (EWA) delivers peace of mind and better budgeting

22% believe that it would give them peace of mind as they wouldn’t have to worry too much about unexpected/unplanned expenses

21% say it would make budgeting easier for them than just getting paid monthly or fortnightly

20% said it would increase their quality of life as they could enjoy more things without worrying about falling short on funds at the end of the month.

A fairer way to get paid 1 in 5 (20%) feel that it is a fair practice that they are able to access payment for the time that they have worked, and nearly 1 in 5 (18%) would actually prefer using this solution to short-term credit.

Reducing reliance on credit

Over 7 in 10 (71%) of those who are using short-term credit believe that an earned wage access solution can help them.

Tip: Earned wage access (EWA) solution is brought to you by the Employment Hero team. Earned wage access provides employees with on-demand access to their pay, allowing them to access up to 50% of their earned wages before payday, capped at a maximum of $250 per week. Since it’s money an employee has already earned, there’s no credit, loan or interest involved.

Earned wage access is an alternative to high-cost credit, payday loans and short-term debt. Learn more.

What now?

As cost of living pressures reach a breaking point, it’s clear everyday Aussies are feeling the pinch. Almost 1 in 2 Australians are struggling to pay for basic necessities like food and rent between paydays, and they’re turning to short-term credit to bridge the gap. For desperate Australians struggling to make ends meet, short-term credit offers a short-term solution —but creates a long-term worry.

With over half of Aussies having missed financial payments at some point, short-term credit costs can quickly add up: late fees and high interest can compound into steep repayments to create a cycle of debt that’s hard to break out of. The result is poor mental and physical health that takes its toll on a personal and professional level.

If this sounds like you, there’s still hope —and proven ways to embrace financial wellbeing. On-demand and earned wage access products like Earned wage access offer a no-credit, no-interest alternative to payday loans and high-interest Buy Now Pay Later options.

Earned wage access provides early access to your earned pay before payday, without the need to turn to expensive, high-interest credit or go into unnecessary debt.

3. Note: This is an example only and is intended to illustrate how credit card debt can compound over time. These figures are based on the Australian Government’s MoneySmart credit calculator, and are correct as of April 2023.

Disclaimer: The information in this article is current as at July 2023, and has been prepared by Employment Hero Pty Ltd (ABN 11 160 047 709) and its related bodies corporate (Employment Hero) . The information in this article is general information provided in good faith without taking into account your personal circumstances, and financial situation or needs, and should not be relied on as professional advice. Some Information is based on data supplied by third parties and whilst such data is believed to be accurate, it has not been independently verified and no warranties are given that it is complete, accurate, up to date or fit for the purpose for which it is required. Employment Hero does not accept responsibility for any inaccuracy in such data and is not liable for any loss or damages arising directly or indirectly as a result of reliance on, use of or inability to use any information provided in this article. You should undertake your own research and seek professional legal, financial and taxation advice before making any important decisions or solely relying on the information in this article.

Read more: How to automate employee onboarding with AI

Read more: How to automate employee onboarding with AI Read more: AI workforce planning: How to future-proof your talent strategy

Read more: AI workforce planning: How to future-proof your talent strategy Read more: How to automate HR processes: a practical guide for employers

Read more: How to automate HR processes: a practical guide for employers