Switching Payroll Providers UK: A Step-by-Step Migration Guide

Published

Switching Payroll Providers UK: A Step-by-Step Migration Guide

Published

Switching payroll providers in the UK can feel like a big undertaking, especially when pay runs have hard deadlines and your team is already stretched. But for most UK SMEs, the decision builds slowly: recurring payroll errors, hours lost to manual admin, mounting compliance pressure and a system that no longer fits a growing headcount.

In this guide, we’ll walk you through what really matters when you switch: why businesses make the move, how to time it well, how to plan the migration, the mistakes worth avoiding and what to look for in a new provider. When you’re ready, you can download our step-by-step payroll migration guide to manage the process with confidence.

Why businesses switch payroll providers

Few UK SMEs change payroll providers overnight. The decision builds quietly, as small frustrations stack up while your team grows. Here are the most common triggers that prompt UK businesses to make the move.

Frequent payroll errors and corrections

Payroll errors are more than a headache. Overpayments hit cash flow, underpayments erode trust and every mistake demands hours of investigation, recalculation and reissued payslips.

When errors become routine, the problem is usually the system, not your team. A platform with automation and built-in error checks catches issues before they reach employees, so you spend less time firefighting.

Too much manual work and double-handling of data

If HR and payroll sit in separate systems, you’re re-keying the same details twice: new starters, pay rises, address or bank changes. Each entry is another chance for something to slip through.

A single source of truth, where a change in HR flows straight through to payroll, removes that risk. If you’re typing the same data into more than one place, your setup is costing you time and accuracy you can’t afford as you grow.

Compliance pressure is mounting

UK payroll compliance rarely stands still. HMRC requirements, pensions auto-enrolment, National Minimum Wage uplifts and changing legislation all move at their own pace.

Tracking every change manually puts the burden on your team and one missed update can carry real consequences. The right provider stays current on your behalf, applying changes automatically so your pay runs stay accurate.

Your tech stack has outgrown your provider

Disconnected tools are a clear sign you’ve outgrown your provider. Maybe your payroll won’t talk to your accounting platform, or your reporting needs a spreadsheet export to tell you anything useful.

These gaps were manageable when your team was small. At 100-plus employees, they create friction across finance, HR and operations. A connected platform that syncs payroll with pension providers, bank deposits and accounting software cuts out the workarounds.

Lack of support when you need it

Payroll runs to hard deadlines, so support has to keep pace. When you’re 48 hours from a pay run and something doesn’t add up, a slow reply won’t do.

Many businesses switch because their provider leaves them stranded at the worst moment. Responsive, UK-based experts who understand payroll and employment law give you a safety net when it counts most.

These triggers rarely appear in isolation. More often they build together until switching becomes the obvious next step. Once you reach that point, the key is timing the move well, which is exactly what we’ll cover next.

When is the right time to switch payroll software?

There’s no single perfect moment to switch payroll software, but some timings make the move far smoother than others. Getting the timing right reduces the data you need to carry across, lowers the risk of errors and helps your first pay run on the new system land cleanly.

Aligning with the tax year end

The start of a new UK tax year on 6th April is the cleanest cut-off point for a switch. At that moment, your year-to-date figures reset to zero, so there’s far less data to migrate and validate. You’re not carrying forward cumulative totals for gross pay, tax, National Insurance or pension contributions, which removes a whole layer of reconciliation.

Practically, this means a lower chance of cumulative calculation errors slipping into your first pay run. It also gives you a natural deadline to plan towards, so you can prepare your data and run your checks ahead of go-live. If you have the flexibility to wait, aligning with the new tax year is the simplest route.

Switching mid-year

Aligning with the tax year isn’t always realistic and that’s completely fine. Most UK businesses switch mid-year and the process works well with the right preparation.

The key difference is that your new provider needs to import accurate year-to-date figures so your end-of-year reporting still adds up. That includes:

- Gross pay to date.

- Tax paid.

- National Insurance contributions.

- Pension contributions.

Before go-live, reconcile these totals against your current system for the same period and investigate any discrepancy straight away. A good onboarding team will guide you through this, so a mid-year switch needn’t feel daunting. Bottom line: mid-year moves are routine, as long as your year-to-date data is accurate and verified.

Signs you shouldn’t wait

Sometimes the right time is now, whatever the calendar says. If your current setup is actively causing problems, waiting until April only prolongs the pain. Watch for these signals:

- Repeated payroll errors: more than one error in recent months points to a system issue, not a one-off slip.

- Growth milestones: you’ve outgrown your headcount tier or your provider can’t support your next stage of growth.

- Manual admin burden: your team spends days rather than hours on each pay run, re-keying data across separate systems.

- A provider that no longer fits: slow support, missing features or no native support for RTI, pension auto-enrolment or HMRC reporting.

When these issues stack up, the cost of staying outweighs the effort of moving. In that case, switching sooner protects both your team’s time and your employees’ trust.

How to plan your payroll migration

A structured plan removes most of the stress. The businesses that struggle with payroll migrations are almost always the ones that skipped the planning stage.

Set clear goals and success measures

Be specific about what you want the new system to do differently. Cutting payroll processing time by 50%, eliminating manual data re-entry, or passing your next auto-enrolment audit without a spreadsheet in sight.

Whatever your goals and success metrics are, write them down. It keeps the project focused and gives you a way to measure whether the switch worked.

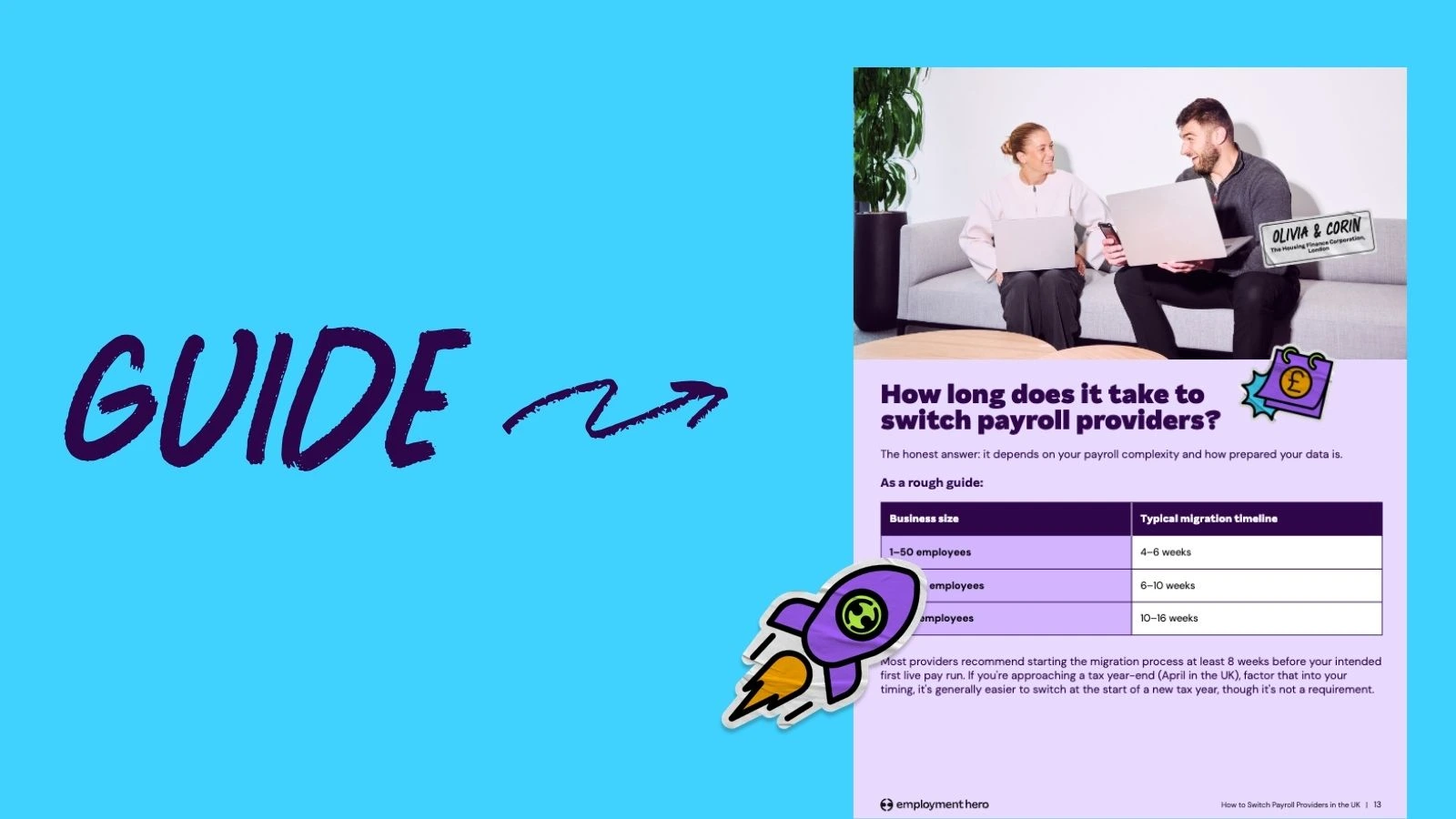

Build your migration timeline

Work back from your chosen go-live date. Most migrations take four to ten weeks depending on payroll complexity and headcount. Build in time for data validation, a parallel pay run and employee communication, not just the technical setup.

Assemble your team and assign owners

This isn’t a one-person job. HR, finance and payroll each have a role. Your new provider’s onboarding team should be in the room (or the call) from day one, not brought in at the point something goes wrong.

Notify your current provider and review your contract

Check your notice period. 30, 60, or 90 days is standard. Confirm data export rights (your payroll data belongs to you), clarify who handles outstanding RTI submissions and P11Ds up to your last pay run and watch for auto-renewal clauses that can lock you in for another year.

The difference a plan makes: A business that migrates without a timeline often finds itself splitting a pay period across two providers, missing a pension contribution deadline, or going live without validating year-to-date figures. A business with a migration plan avoids all three.

Common payroll migration mistakes to avoid

Most migration problems come from a handful of avoidable mistakes. Once you know where things tend to go wrong, they’re far easier to sidestep. Here are the five pitfalls to watch for.

Rushing the data transfer

Skipping validation to hit a deadline is the fastest route to errors on day one. Inaccurate tax codes, pay rates or year-to-date figures simply carry forward and surface in your first live pay run.

Build validation time into your timeline. Reconcile gross pay, tax, National Insurance and pension contributions against your current system before go-live.

Skipping the parallel run

A parallel run means processing the same pay period in both systems and comparing the results line by line. It can feel like double the effort, which is why some teams are tempted to skip it.

Don’t. It’s the most effective way to identify discrepancies before they reach employees’ payslips. A parallel run can also uncover compliance risks, highlight data or process issues and provide an opportunity to review how payroll is managed. This allows your implementation team to recommend improvements and streamline processes before go-live, helping you transition with confidence.

Poor software setup

Misconfigured pay conditions, incorrect tax settings or missing pay schedules are usually the result of rushing through setup alone and they’re surprisingly disruptive once pay runs begin.

This is where guided onboarding helps. A provider with a dedicated implementation team gets everything configured correctly from the start. Use the support on offer rather than going it alone.

Forgetting to test integrations

Your payroll needs to connect cleanly with your pension provider, bank payment system and accounting software. Untested integrations have a habit of failing at the worst moment.

Before go-live, confirm each connection works end to end:

- Pensions: Check that contributions are submitted correctly in the format your provider accepts.

- BACS payments: Verify that BACS files generate and process as expected.

- Accounting: Make sure payroll data flows through without manual exports.

Leaving employees in the dark

A payslip that suddenly looks different, with no warning, guarantees a wave of questions to HR. Most of that is avoidable with a short message before your first live pay run.

Tell your people what’s changing, such as a new payslip format and what isn’t, like pay dates, amounts and bank details. A little communication upfront saves you time later.

What to look for in a new payroll provider

Choosing the right provider matters just as much as planning the move itself, so look for these features to make sure your next payroll system supports your team today and scales with you tomorrow.

- Integrated HR and payroll in one platform: When HR and payroll share a single source of data, you eliminate double-handling and the errors that come with it. Changes to employee records update payroll automatically. No re-keying required.

- Automation and built-in error checks: Automated pay runs with validation alerts catch issues before they reach your employees. That’s time saved and errors avoided on every single pay run.

- Compliance support that keeps pace with legislation: HMRC changes, NMW uplifts and auto-enrolment updates shouldn’t require your team to manually track and apply them. Your provider should handle it.

- Seamless integrations: Pension providers, bank payment systems and accounting software should connect without manual exports in between.

- Responsive UK-based support and onboarding: You need to reach a real person when a pay run is at stake. Check SLAs, support hours and how onboarding is structured before you commit.

- Scalability for a growing business: A system that works at 20 employees needs to keep working at 150. Check headcount tiers, feature availability at each tier and whether the pricing model makes sense as you grow.

Ready to make the switch?

Switching payroll providers is manageable when you go in with a plan. Get the data right, validate before you go live, choose a provider that grows with you and the transition is far less disruptive than most businesses expect.

Employment Hero brings HR and payroll together in one platform: automated pay runs, built-in error checks, HMRC and pension integrations and UK-based support throughout your migration and beyond.

Want to find out more?

Disclaimer: The information in this article is current as at June 2026, and has been prepared by Employment Hero Pty Ltd (ABN 11 160 047 709) and its affiliates (Employment Hero). The views expressed in this article are general information only, are provided in good faith to assist employers and their employees, and should not be relied on as professional advice. Some information is based on data supplied by third parties. While such data is believed to be accurate, it has not been independently verified and no warranties are given that it is complete, accurate, up to date or fit for the purpose for which it is required. Employment Hero does not accept responsibility for any inaccuracy in such data and is not liable for any loss or damages arising directly or indirectly as a result of reliance on, use of or inability to use any information provided in this article. You should undertake your own research and seek professional advice before making any decisions or relying on the information in this article.

Frequently Asked Questions

Four to ten weeks is typical for most UK SMEs, depending on payroll complexity and headcount. Larger businesses or those with multiple pay frequencies, pension schemes, or complex pay structures should allow more time. Starting at least eight weeks before your intended go-live date gives you enough runway for data validation and a parallel pay run.

With a well-managed migration, employees shouldn’t experience any disruption to pay dates or amounts. What they will notice is a new payslip format or self-service portal, which is why communicating the change before it happens matters.

Yes. There’s no HMRC rule against it. You’ll need accurate year-to-date figures (gross pay, tax, NI, pension) migrated into the new system so that end-of-year P60s and P11Ds are correct. Most providers have a structured process for mid-year migrations.

Your payroll data belongs to you. A reputable provider will export it in full on request. You’re legally required to retain payroll records for three years from the end of the tax year they relate to, so make sure you have copies before access to your old system is removed.

Notify your pension provider before go-live and confirm the contribution file format your new system will use. For HMRC, your PAYE reference stays with your business, your new provider configures their RTI submission software with your existing scheme details. No gap in RTI reporting is the goal; your migration timeline should be built around that.

Register for the Step-by-Step Migration Guide

Related Resources

-

Read more: Employer Playbook: What is onboarding?

Read more: Employer Playbook: What is onboarding?Employer Playbook: What is onboarding?

Real onboarding starts at offer acceptance, spans 90 days and is the #1 source of HR errors. Here’s how to…

-

Read more: Employment Contracts UK: What Employers Are Legally Required to Include in 2026

Read more: Employment Contracts UK: What Employers Are Legally Required to Include in 2026Employment Contracts UK: What Employers Are Legally Required to Include in 2026

Employment contracts UK rules are changing under the Employment Rights Act. Find out what to include and update before 2026.…

-

Read more: Switching Payroll Providers UK: A Step-by-Step Migration Guide

Read more: Switching Payroll Providers UK: A Step-by-Step Migration GuideSwitching Payroll Providers UK: A Step-by-Step Migration Guide

Thinking about switching payroll providers? Learn when to switch, what to plan for, common migration mistakes, and what to look…