What Is Bookkeeping? An Introduction for SMBs

Small business bookkeeping can be a bit of an enigma. The good news is, you’re not in it alone – there are tools out there that make bookkeeping much less daunting and scary.

-

The Team

Last Updated

18 mins read

Starting your own business is an exciting time. No doubt you’ve been looking forward to engaging with your new customers and begin turning a profit. However, you may be feeling a little less keen to start bookkeeping, especially if you’re not much of a “numbers person”.

Luckily, you don’t have to do it alone. With access to the right bookkeeping tools for your business or help from an expert, you don’t need to be a finance whiz.

You’re probably wondering, “should I hire a bookkeeper?” The short answer is probably.

However, you can choose to manage the books yourself. Whether you decide to outsource the job or tackle it on your own, all SMB owners should learn the basics of bookkeeping.

Having a general understanding can help steer your business in the right direction and avoid running into any cash flow or tax-related roadblocks.

Bookkeeping definition

In a nutshell, bookkeeping refers to the recording and classification of all financial transactions within your business. It involves documenting precisely what you spend and earn. A bookkeeper is a person responsible for managing that process.

Without detailed bookkeeping, it can be difficult for a business to see if they’re profitable. Watching over your numbers can help to identify any financial challenges that may hinder progress.

Bookkeeping also provides an opportunity for businesses to identify areas in which they can expand, areas that might not have otherwise been noticed without clear financial reporting.

For a deeper understanding of financial responsibilities, read our guide on Australian business tax.

The most common financial transactions for bookkeepers:

- Invoices from goods or services

- Recording any invoices owed to external contractors, suppliers etc.

- Payments to contractors, suppliers etc.

- Tracking employee payroll

- Paying employees

- Recording payroll taxes

- Preparing financial reports

- Handling bank financial statements

- Providing financial information to an accountant for analysis

An intro to bookkeeping basics for SMBs

Here are key bookkeeping concepts and definitions essential to understanding the methods and processes bookkeepers use to maintain accurate accounts:

- Accounts: Categories used to classify all business transactions.

- Assets: Items the business owns or partly owns, such as inventory, property, or money owed to the business (accounts receivable).

- Balance Sheet: A snapshot of the business’s assets, liabilities, and their values at a specific point in time.

- Chart of Accounts: A comprehensive list of accounts used to track financial transactions in the ledger, also known as general ledger codes.

- Equity: Funds introduced or withdrawn by the owner or shareholders.

- Expenses: Money spent to maintain and operate the business.

- Financial Statements: Reports summarising a business’s financial activities and performance, primarily the balance sheet and profit and loss statement.

- Ledger: A record where business transactions are logged and categorised.

- Liabilities: Amounts the business owes, including unpaid bills, taxes, wages, or loans.

- Profit and Loss (P&L) Statement: Summarises revenue and expenses over a period, showing the business’s profitability.

- Revenue: Income generated from sales, interest, or dividends.

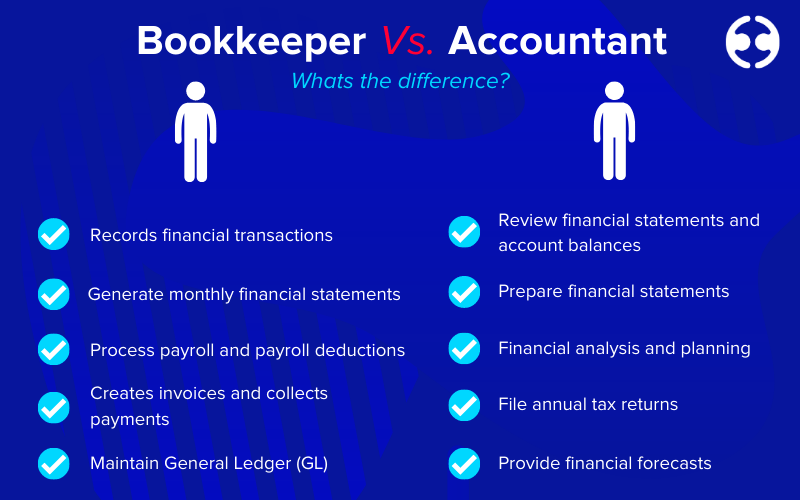

Bookkeeping vs Accounting

If you’re already savvy with some basic accounting terms, you’re probably wondering how an accountant’s job differs from a bookkeeper’s. Some people may use the words interchangeably. While the two roles go hand in hand, they each have their own distinct job function.

Bookkeeping involves recording and classifying financial transactions within a business, whereas accounting focuses on reviewing, analysing and interpreting the data bookkeeping provides.

What do the experts think?

So to clarify, bookkeepers have a transactional role that is mostly administrative. Whereas an accountant’s role is considered to be more subjective, as their insights and analysis are provided through bookkeeping data.

Why is bookkeeping important for SMBs?

If you’re in the early days of running a business, now is the perfect time to learn about the importance of managing your books.

For any small business, bookkeeping is essential for long-term success. It’s important to have an accurate insight into the financial ins and outs so you can make more informed business decisions. Understanding where you stand financially will determine where your business will go in the future.

Detailed bookkeeping can also protect your business. Without any clean financial records, you risk skipping over any financial errors.

In the unfortunate event of a customer, supplier or employee committing fraudulent activity, accurate reporting can help to prevent or uncover this. Businesses are also obligated by Australian Law to supply up-to-date financial records for levy and tax purposes. Not to mention, bookkeeping can help you save valuable time.

From invoicing to managing payroll, financial reporting keeps you on track with your business earnings and expenses, so you don’t need to waste any time tracing each transaction.

Why do you need to record financial statements?

- To make sure you’re spending less than you’re earning

- For reliable financial reporting that helps with budgeting decisions

- Stay on top of any invoices to or from suppliers, contractors etc.

- To manage expected payments from customers

- Prevent any incorrect payments that can cost the business money

- To complete accurate tax returns

- Ease of transferring financial information between accountants or investors

Understand the most common business accounts

In the art of bookkeeping, an account refers to a specific record of financial transactions, e.g. payroll or utilities. If you’re new to bookkeeping, it’s important to be aware of the various business accounts you will likely engage with.

The five most common accounts are:

- Assets – what the business owns (e.g. accounts receivable, inventory)

- Liabilities – what the business owes (e.g. accounts payable, loans)

- Income or revenue – money earned by the business

- Expenses – the cash that flows out from a business to pay for an item or service (e.g. salaries, utilities)

- Equity – the value remaining after liabilities are subtracted from assets, representative of the owner’s or an investor’s held interest in the business (e.g. stock, retained earnings)

Bookkeeping starts with establishing each necessary account for your business. After which you may begin recording each transaction in the relevant category.

Accounts may differ between each business. However, the most common types remain the same.

Outsourcing SMB bookkeeping

If you’re a start-up or SMB owner, you may decide to start with managing your own books. As your business begins to grow, you will more than likely need to outsource your bookkeeping. Bookkeepers provide various different service levels which cater to your current budget.

This way you can start with the basics and then add on additional services as you continue to expand.

How does software help?

If you’re after a more cost-effective solution to hiring a bookkeeper, then bookkeeping software is your answer. These virtual records help minimise the costs and time associated with financial reporting, all the while keeping your business on track.

Bookkeeping tasks traditionally were managed through books and ledgers. Transactions were recorded in physical daybooks or journals and then transferred to the general ledger (main accounting record).

Nowadays, bookkeeping software is available to speed up financial reporting, remove human error and help with audit trails.

There are two common methods for building a virtual general ledger (GL):

- Basic: spreadsheet software (e.g. Microsoft Excel)

- Advanced: cloud-based payroll software (e.g. Employment Hero)

Naturally, the most affordable option would be spreadsheet software such as Google Sheets. However, structuring your own GL in a spreadsheet program can be a challenging task.

Although online cloud-based software often requires a monthly subscription fee, these programs help to crunch numbers and track financial data in real-time so you can focus on growing your business.

The wrap up

Whether you decide to tackle the books yourself, outsource to an industry expert or subscribe to bookkeeping software, having an understanding of the basics will help you stay on top of your business’ finances and make more informed decisions in the future.

Bookkeeping can save time chasing every dollar and protect your businesses from any financial errors. Although bookkeeping may sound like a tedious task, it certainly doesn’t have to be.

Want to take your business to the next level? Check out our small business owner’s guide to networking. With the right tools and understanding of each relevant account, you’ll find the process to be highly useful for future planning and decision-making.

Disclaimer: The information provided in this article is general in nature and is not intended to substitute for professional advice. If you are unsure about how this information applies to your specific situation, we recommend you contact a professional for further advice.

Related Resources

-

Read more: How to automate employee onboarding with AI

Read more: How to automate employee onboarding with AIHow to automate employee onboarding with AI

Learn how to automate employee and client onboarding using AI, HR software and workflows to improve efficiency, compliance and experience.

-

Read more: AI workforce planning: How to future-proof your talent strategy

Read more: AI workforce planning: How to future-proof your talent strategyAI workforce planning: How to future-proof your talent strategy

Explore how AI is transforming workforce planning, from forecasting talent needs to identifying skills gaps and modelling future workforce scenarios.

-

Read more: How to automate HR processes: a practical guide for employers

Read more: How to automate HR processes: a practical guide for employersHow to automate HR processes: a practical guide for employers

HR automation can save your team hours every week. Learn which HR processes to automate first, how to implement HR…