A guide to employer KiwiSaver contributions

Published

A guide to employer KiwiSaver contributions

Published

Managing KiwiSaver contributions is a key responsibility for New Zealand employers. The scheme itself affects payroll, compliance and your team’s long-term security. For many businesses, contributing to KiwiSaver is more than a deduction as it can have an impact on staff trust and retention.

Our guide offers clear, practical support. You’ll find step-by-step advice on your obligations, calculation methods and managing filing, with examples and links to help you through common scenarios.

Why understanding employer contributions matters

Administering KiwiSaver correctly helps your business run smoothly and demonstrates that you value your employees. Mistakes can lead to back-payments, unhappy staff or attention from Inland Revenue. For fast-growing businesses, you may find the process soon grows in complexity. Addressing it early offers you the reassurance that your payroll and administration meet New Zealand requirements. Strong KiwiSaver processes also help present your workplace as reliable and attractive when you’re trying to recruit or retain staff.

What employers need to know about KiwiSaver

You act as the link between your employee and their retirement savings -collecting, calculating and filing both your own and their contributions. This may seem simple, but the detail matters. Eligibility, ESCT tax rates and filing deadlines all need careful handling.

What is KiwiSaver?

KiwiSaver is a voluntary work-based savings scheme set up by the New Zealand government, mainly intended to help people save for retirement. While joining KiwiSaver is voluntary for employees, you as the employer have a responsibility to facilitate it for eligible staff.

Most employees join hoping to secure their retirement but KiwiSaver funds can be accessed for a first home purchase as well, making it relevant across your team’s life stages. The government offers annual contribution incentives directly to employees.

How does KiwiSaver work for employees and employers?

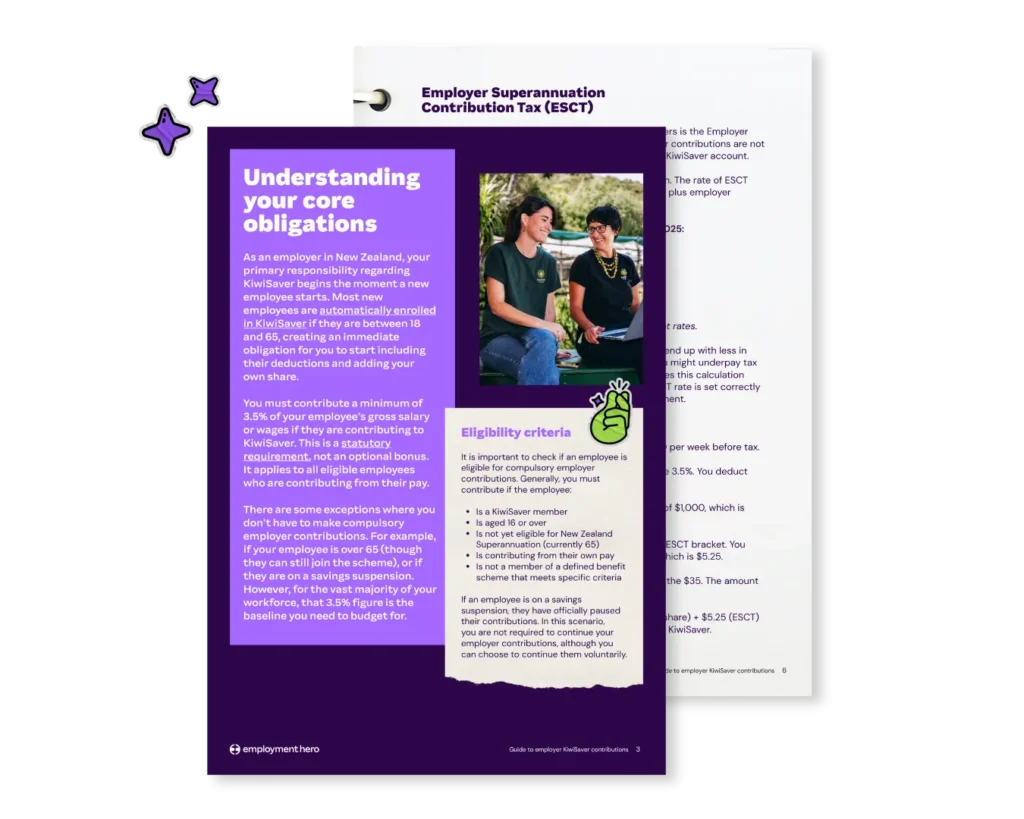

Employers must enrol new eligible staff (unless they are already members or are exempt), then deduct the contribution rate the employee chooses. Most commonly this is 3.5%, 4%, 6%, 8% or 10%. You also calculate and add your minimum required contribution on top. The minimum contribution for employers is currently set at 3.5%.

Alongside the rest of your employment information, all amounts are reported and paid to Inland Revenue each pay cycle. From there, Inland Revenue sends the funds to your employee’s selected fund provider. Apart from forwarding the correct information and money to Inland Revenue, you do not need to handle any investment decisions.

Are employer contributions to KiwiSaver compulsory?

Employer contributions are compulsory for the majority of your staff. If an employee is contributing, you must contribute too.

There are a few exceptions. Currently if the employee is over 65, you don’t have to make compulsory contributions, although you can choose to. Employees who are not KiwiSaver members, are on a savings suspension or participate in an alternate defined benefit scheme may also be exempt. Checking eligibility for each new starter is essential to avoid problems later.

How much do employers have to contribute?

The minimum you must contribute is 3.5% of the employee’s gross salary or wages. Gross pay covers base wage, overtime, commission, bonuses and all leave payments. It excludes genuine reimbursements, redundancy payments and accommodation value.

Your contribution is assessed on the total before tax, but before payment to a KiwiSaver provider, you must also deduct Employer Superannuation Contribution Tax (ESCT), so your employee’s fund will only receive what’s left after tax.

Voluntary contributions as a retention strategy

Sticking to 3.5% is standard but considering a higher contribution can make a real difference in a tight job market. Matching an employee’s 4% or higher can set your business apart, offering a strong incentive for both candidates and existing team members. It can even be used when negotiating with senior hires or to retain valued long-term staff.

Some employers continue contributions for staff over 65, or during periods of unpaid leave, as a way of demonstrating goodwill. These choices support stronger engagement and can be a valued part of your workplace culture.

Can employers deduct KiwiSaver contributions from employees’ pay?

It is important to be clear: employee contributions are deducted from their pay, as savings for their future. Employer contributions, by contrast, are paid by you, as an additional cost on top of their wages. You are not allowed to deduct your own portion from an employee’s net or gross pay.

However, there is one exception. If a remuneration package is agreed as “total remuneration” and the agreement clearly states KiwiSaver is included, your contribution can be factored into the agreed sum. Where the contract wording is unclear, you may find yourself liable for more than intended. Reviewing contract templates, or seeking advice, is recommended if using total remuneration structures.

What happens if employers don’t pay KiwiSaver contributions?

Not fulfilling your KiwiSaver duties is a breach of New Zealand employment law. Inland Revenue treats unpaid KiwiSaver as it would unpaid tax, and has the powers to take action or collect debt. Failing to pay may also lead to penalties, late payment interest, or employee grievances, which can escalate to mediation or more. It may also cost your reputation, as news of underpayments spreads quickly across industries.

If you discover a shortfall, it’s best to contact Inland Revenue for advice and consider voluntary disclosure. Proactive correction is often viewed more favourably than waiting for an audit or employee complaint.

How to set up KiwiSaver for your business

Setting up as a KiwiSaver employer happens automatically when you register as an employer with Inland Revenue and for PAYE.

From there:

- Choose and check your payroll software, ensuring it correctly manages KiwiSaver calculations and filing (Employment Hero’s payroll software is set up for this!)

- Provide new staff with KiwiSaver deduction and employee details forms (KS2 and KS1) as part of your onboarding

- Confirm eligibility for automatic enrollment as each new employee joins

- Record tax codes and ESCT rates accurately

Manual payroll calculation increases the risk of errors, so using specialist payroll software is strongly recommended. This can help with keeping your records up to date with changes from Inland Revenue and MBIE.

Paying KiwiSaver contributions as an employer

You don’t pay KiwiSaver funds directly to a provider. Combining all your payroll deductions, student loan payments, employer and employee contributions, you pay one combined sum to Inland Revenue after each payday filing.

Depending on how much you pay in PAYE overall, you will do this either monthly or twice a month, with the deadlines set by Inland Revenue. The department then distributes the correct amounts to the providers for each of your employees. This system frees you from having to track multiple providers or accounts.

How to calculate KiwiSaver contributions

Calculating employer contributions always starts with 3.5% of gross pay. Once you have the number, calculate ESCT and deduct it from the sum before transferring the rest to your employee’s fund. Your employee’s ESCT rate depends on their total salary, plus employer contributions for the year.

From 31 March 2025, ESCT rates are:

- Income up to $16,800: 10.5%

- Income from $16,801 to $64,200: 17.5%

- Income from $64,201 to $93,720: 30%

- Income from $93,721 to $216,000: 33%

- Income over $216,000: 39%

Who are the registered KiwiSaver providers?

Employees are entitled to choose their own provider from a list, including high street banks, investment groups and boutique managers. If no provider is selected, Inland Revenue assigns one by default. You don’t need to give recommendations or hold a list of providers. In fact, employers must maintain neutrality on provider choice.

Understand the basics of KiwiSaver contributions with our guide

As an employer, it’s critical that you understand what is required of you with each pay run. Understand the key information about KiwiSaver employer contributions with our guide. Download the guide by filling in the form on the right.

The information in this article is current as at 30 December 2025, and has been prepared by Employment Hero Pty Ltd (ABN 11 160 047 709) and its related bodies corporate (Employment Hero). The views expressed in this article are general information only, are provided in good faith to assist employers and their employees, and should not be relied on as professional advice. Some information is based on data supplied by third parties. While such data is believed to be accurate, it has not been independently verified and no warranties are given that it is complete, accurate, up to date or fit for the purpose for which it is required. Employment Hero does not accept responsibility for any inaccuracy in such data and is not liable for any loss or damages arising directly or indirectly as a result of reliance on, use of or inability to use any information provided in this article. You should undertake your own research and seek professional advice before making any decisions or relying on the information in this article.

Register for the guide

Related Resources

-

Read more: AI training at work: who’s responsible, you or your staff?

Read more: AI training at work: who’s responsible, you or your staff?AI training at work: who’s responsible, you or your staff?

Kiwi workers uniquely expect employers to lead AI training. Here is why the responsibility sits with you, plus a 90-day…

-

Read more: AI guilt at work: the hidden productivity drag nobody’s talking about

Read more: AI guilt at work: the hidden productivity drag nobody’s talking aboutAI guilt at work: the hidden productivity drag nobody’s talking about

More than a third of NZ workers feel guilty using AI well. That guilt quietly drags on output. Here is…

-

Read more: The NZ SME AI gap: why Kiwi businesses are behind Australia and what to do about it

Read more: The NZ SME AI gap: why Kiwi businesses are behind Australia and what to do about itThe NZ SME AI gap: why Kiwi businesses are behind Australia and what to do about it

New Zealand workers are the most AI-ready of any market, yet Kiwi SMEs trail Australia on adoption. Here is why…