Key learnings from the Accounting and Finance Show 2023

Discover valuable tips and insights that will help in shaping your practice management strategies for the future.

-

Carissa Ng

Published

Updated

22 mins read

Contents

Last week, we had the pleasure of attending the Accounting and Finance Show in Singapore — held on 10th and 11th October at the Suntec Convention Centre.

It was a power-packed two day event, and our team had a great experience chatting to every single one of you who came to say hello and learn more about Employment Hero. More importantly, we hope you love the notebook packs we gave out, as well as our caricature artist who drew lifelike portraits of you, your partner, or even your pet on our branded mugs!

We had access to 5 content theatres where we gained lots of valuable insights from industry leaders. From panel discussions to engaging presentations, a core theme that emerged across both days was the need for digital transformation, and managing your growing tech stack effectively.

Regardless of whether you attended the event or not, we hope you’ll find these key learnings thought-provoking and influential in shaping your practice management strategies for the future.

1. App stack and app advisory for smaller practice firms

In a panel discussion moderated by Heather Smith, with speakers Tang Shiuh Huei, Kyelie Baxter, and Samuel David, they shared lots of great tips on how to manage your tech stack effectively.

When assessing if a tech solution is the right fit, here are some considerations you should have:

- Is it solving a problem?

- Does it overlap with a solution you’re already paying for?

- What training costs will it entail?

- How will the change management process be like?

- Does it fit with your current app stack?

It’s important to test out the tech first before implementing them for your clients, to ensure that it harmonises with the current workflow and ensures a more seamless transition.

If you’re offering tech advisory services, scoping the project and ensuring that expectations are met on both sides is the most challenging part. Here are some tips to help you out:

- Spend time talking to your clients and find out what they want.

- For newer applications, do your research thoroughly and take time to understand them first.

- Offer your clients a clear, visual representation of each tech solution — with so many tech options available in the market, it can get very overwhelming and confusing for them.

- Find the app that is most applicable to your client’s needs and pain points.

- Consider the two groups of employees on your client side — the decision makers (i.e those who are paying for it), and the operational side (i.e employees who will be using it).

And when it comes to implementation, what should you look out for?

There are 3 parts to a successful implementation — the trial period, the optimisation period, and the monitoring period. The trial period is when you take the app for a test drive, and show your clients what goes on behind the scenes. Once your clients are happy with it, you then fine tune and optimise the workflows to ensure that everything works smoothly and efficiently. Last but not least, monitor the progress and analyse all the data that is coming through — you’ll want to be making sure that your client is happy with the product and that you don’t run into any hiccups using the app.

Another tip the panel provided was to do beta testing, and run the app with a small number of clients from diverse industries and backgrounds. Use it to find out what they like or don’t like about it so you can make a more informed decision, before you decide to roll it out to all your clients.

In addition, make sure you have weekly meetings with your clients during the implementation process, so they are constantly kept up to date with the progress. Sometimes there might be a disconnect between client expectations and what the product actually does, so it’s best to iron out any misconceptions as soon as possible. It’s also crucial to create a handbook for your clients so all the processes taken in the implementation journey are outlined clearly, and they have a source of truth to follow.

When it comes to partnering with tech vendors, here are some questions you should be asking them:

- How much support will be given? (This is crucial in being able to carry out a successful implementation.)

- Where is the data stored? (Data security is a huge concern at the moment.)

- What’s on the roadmap? (Your clients might have specific pain points they are struggling with at the moment, but you can assure them by letting them know that certain features are due to be released soon.)

- Do you have a case study? Can I have some examples of clients you have?

- Are you connected to an API solution?

How should you go about reviewing and refining your tech stack?

- Keep up with new applications that are released in the market.

- Gain valuable insights from your implementations process, which will inform your perspectives on what you want and don’t want from your tech stack.

- If you manage to find a better app, bring it up to your clients as recommendations.

- Focus on what pain points your clients have, and whether there is a better solution available for them.

- Don’t just set and forget—your tech stack needs to be regularly reviewed and assessed!

- Do a cost and benefit analysis so you can assess different factors and have a more multifaceted overview.

- Share your tech stack with others on social media and get them to critique it—you’ll be surprised at how useful it can be!

What are some mistakes smaller firms make when implementing tech?

- Clients may not understand the tech solution sufficiently—they need to know that it’s a constant learning process that they need to keep up to date with.

- Clients often believe that once the system is in place, they don’t need to do anything or conduct regular checks, but that’s not true at all.

- You need to ensure that you are asking as many questions to your clients as you can—often, the people using the tech solution know the processes better than the decision-makers at the top who are paying for it. Get a complete consultation of all levels on the client side so you can better assess the needs they have.

How do you juggle the deadlines and process of transiting to a new software from an old software?

- Do it module by module, step by step.

- Keep both the old software and new software running simultaneously for a short period of time to ensure a smooth transition.

- Be honest and real with your clients—it’s going to be a painful process, but the long term benefits are worth it.

- Test the new software out on a trial basis first—use sample data and get approval from your client to do so.

Ultimately, the 3 key takeaways are:

- It’s important to work on solving your client’s problems, rather than forcing your perspectives on clients.

- The future is big and great—with technological advancements, so many products and features are constantly being released. Ask your vendors more questions.

- Having the ability to connect and work with software providers is key—a good relationship helps with transparency and collaboration.

2. Balancing your workplace: people, systems and technology

In a world of work that is constantly evolving and changing, Zac Hayes from Ignite Strategy and Tax shared a useful framework that will help you empower your team, motivate the people behind the numbers, and use technology to propel your business to achieve your goals.

That framework is also known as EBITDA—which stands for engagement, belonging, innovation, trust, dreams, and accomplishments.

- Engagement

Let’s start on engagement. How do you put it into practice? Zac espoused that it’s all about having a clear and compelling purpose—and singing it from the rooftops, both internally and externally. He emphasised that it’s important to practice strength spotting and coaching—make sure you know your own strengths, focus on other people’s strengths, and mindfully observe behaviours to identify strengths in others for coaching purposes. There’s a free online strengths tool called VIA Strengths which you can use to assess.

It applies to hiring as well—use strength-based interviewing so you can focus the interview around a positive conversation as opposed to a sense of inspection. Ask questions that allow the person to highlight their naturally occurring strengths, such as “What are you most proud of? What energises you? Describe a time when you were at your best.” Not only will you enjoy the conversation a lot more, you’ll also be able to assess the strengths of the candidate and how well it matches their role. This is a much better indication of their ability to flourish rather than focusing on their experience and qualifications.

- Belonging

Do you value the work your employees are doing? How do you make work fun? Ensure your values are clear and unique to your culture, and hire your team based on these values. Your values will become the guiding light in your organisation for decision-making, providing a common language, and evoking a sense of belonging.

In addition, run unconscious bias training—help all employees, particularly leaders and managers, uncover any unconscious bias that could be hindering greater diversity and inclusion around recruitment, promotions and other important decisions. We all have them, but because they are unconscious you often don’t know that they are there and need to be worked on. You can create your own training modules, or leverage online modules such as this one from Facebook.

- Innovation

It’s important to build innovation into all areas of your business. You may hit your KPIs today, but the industry is ever-evolving. How are you going to solve the problems of tomorrow?

Foster innovation by giving people the time to do it, and create environments that inspire it. For example, you could incorporate walk and talk meetings out of the office to enhance physical and intellectual capacity, creating new neural pathways in the brain. Alternatively, you could kick off a meeting with an innovation game or exercise to get people to think differently. You could also create offices that encourage play, such as having a basketball hoop, table tennis, foosball table and more around.

Use ‘design thinking’ to leverage intuition and empathy, to reframe a problem which will lead to many more solutions. Get teams together to brainstorm and encourage equal participation from all personality types—you won’t always hit the innovation jackpot, but even one new idea could result in the transformation your business needs to set it apart.

- Trust

Communication is key in a business—so find the best digital tools that your teams can use to make communication easy. However, these should not replace the value of having face to face conversations. Be open, transparent and share as much as you can about your business. Knowledge is power, so share that power with others who can help grow your business!

As leaders, you can also admit that you don’t have all the answers, make mistakes, and ask people for help. It’s ok to be vulnerable. Not only does this build trust with your team, it also makes your life far less stressful when you’re being authentic and honest.

Listen to what people have to say—this could be from a regular engagement survey where people can provide feedback anonymously, and respond and take action whenever needed. It’s also crucial to show empathy, gratitude and compassion—remember to appreciate others show them that they are valued.

Some of these actions may seem small, but they are a powerful way to build trust and enhance employee wellbeing. As we all know, having quality connections and relationships are the biggest contributors to enhancing the wellbeing of everyone.

- Dreams

With Generation Alpha joining the workforce soon, it’s important to note that they won’t be staying loyal to one company their whole lives. They will be loyal to the answers they get—like the vision and mission of your business, what greater purpose you’re contributing towards, and how they can be a part of that.

That’s exactly why it’s important to take time out from ‘business as usual’ tasks to dream. Bring the dreamers together in your business, look 2 years ahead and ask questions like “What is good? What is right? What is possible?” Ignore any obstacles or limitations for the moment and just imagine the possibilities. These will give you the courage to pursue bigger goals and dreams, and have a stronger vision in mind for the future.

- Accomplishments

Set performance and learning goals—they give a tangible sense of accomplishment, and encourage a growth mindset. Even if you fail at something, at least you tried something new and stepped out of your comfort zone. It’s still an achievement worth celebrating.

More importantly, remember to have celebrations along the way. Give your employees recognition where it’s due. Recognising and appreciating employees for their contributions can help to boost their motivation and engagement. When employees feel valued and appreciated, they are more likely to be committed to their work and the organisation. They will also be motivated to perform their best when they know their efforts are acknowledged and rewarded.

All in all, people are the foundation for any business—and by using this EBITDA framework, you can ensure that your team thrives and achieves their goals.

3. What’s next for accountants in Southeast Asia?

What does the role of a Southeast Asia-based accountant look like now, and in 5, 10 and 20 years? Gin Toh, from the Institute of Management Accountants, shed some light on how the role is forecasted to change, how innovative technologies will impact that role, and the skills accountants will need to develop in order to stay ahead.

According to Forbes, “tomorrow’s accountants may play an advisory role, welcoming business intelligence and procurement professionals and working to chart a strategic sourcing plan. They could leverage data management tools, including augmented reality, to humanise and contextualise spend data for the C-suite to make better decisions, based on long term value rather than investment alone.”

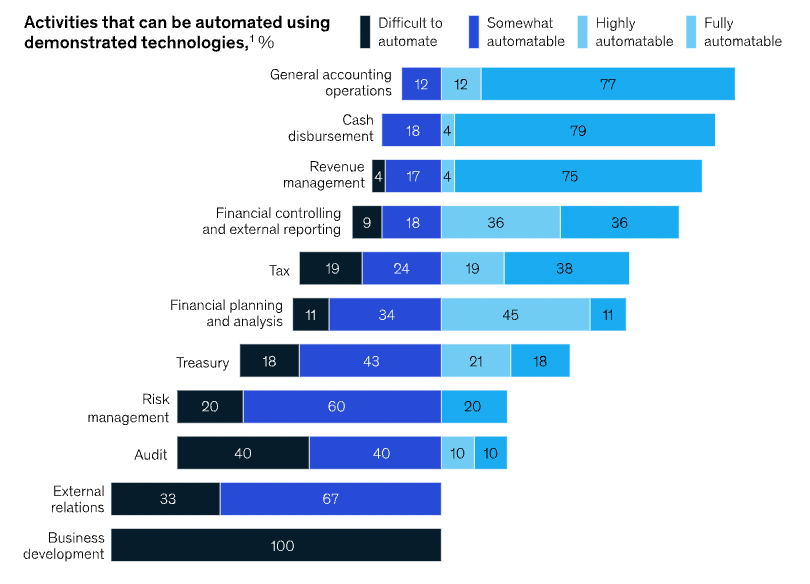

There are many finance tasks that can be taken over by automation, from performing and documenting account reconciliations to financial planning and analysis. A McKinsey study showed that transactional activities are the most automatable, but the opportunities to automate are across all subfunctions.

What does this mean for the accounting role then, especially since ChatGPT successfully passed the CPA exam? Everyone knows the relevance of AI, but most of us don’t have to skills to use it effectively yet. Emerging technologies are advancing rapidly, and new competencies like data analytics are advancing. There is a greater need to speed up the pace of upskilling to leverage these new technologies.

What then, can technology not take over? It is an accountant’s ability to analyse and connect the dots. Rather than focusing on transactional tasks which can be left to automation, focus on efficiency and compliance. Be responsive, insightful and efficient. It’s all about using data analytics to create value for the company, in tangible and intangible ways. Data is the new electricity—without data, you’d be helpless and unable to do anything.

Southeast Asia is one of the world’s most diverse regions, with 11 countries, more than 650 million people, and over 1000 languages spoken. We have a young and entrepreneurial population, with more than half under 30 years of age, and are embracing digital transformation. We also have a vibrant digital ecosystem, with more than 400 million internet users and over 10 unicorns in sectors such as e-commerce, fintech, ride-hailing and gaming. We’ve also got a strategic location connecting China, India and Australia, benefiting from the ASEAN Economic Community (AEC) and the Regional Comprehensive Economic Partnership (RCEP).

But while those factors showcase our uniqueness, our region faces multiple challenges too. There are various restrictions and regulations that differ across regional and local levels, such as intellectual property registration, brand protection, and so on. Recruitment difficulties are rampant, as there is a mismatch between the skills demanded by employers, and the skills available in the labour market.

We are also a fragmented region, as each country has its own unique characteristics, preferences and behaviours. Businesses need to tailor their offerings and strategies to each local context. Our region requires building trust and relationships with local stakeholders, such as government agencies, customers, suppliers and employees. It also demands cultural sensitivity and awareness, as there are many variations in language, religion, customs and norms across the region.

Nevertheless, Southeast Asia holds great growth potential. It’s set to become the world’s 4th largest economy by 2030, with a vibrant innovation ecosystem and an increasing number of unicorns emerging in the region since 2012. A strong regional integration with the ASEAN Economic Community (AEC) and the Regional Comprehensive Economic Partnership (RCEP) enhances trade and investment flows.

There’s also a green growth opportunity, with increasing awareness and action on environmental issues. The region has abundant renewable energy resources that can help reduce carbon emissions and create new industries. In addition, the region’s internet economy is projected to grow from $100 billion in 2019 to $300 billion by 2025. Business activity in the region is also rapidly increasing due to geopolitical tensions—businesses are looking for safe regions to expand into, such as Southeast Asia.

Now that you’ve gotten a better understanding of the region and where we’re headed, there are 2 areas to call out:

Green finance has been on the rise. It refers to financial products, services and investments that support environmentally sustainable and socially responsible projects and businesses. It aims to promote economic growth while addressing environmental challenges. Some examples include green bonds, sustainable investment funds, green loans, carbon markets and green insurance. It encourages the spread of technologies and the development of environmentall infrastructure.

Additionally, a growing area of accounting is forensic accounting—the approach to accounting which utilises accounting, auditing, and investigative skills to conduct an examination into the finances of an individual business. It’s becoming increasingly important because of technological advancements, and the rise of scams and frauds.

With that said, these are the six megatrends for the future of accounting:

- Remote work will become the norm.

- Environmental, social and governance (ESG) reporting will become more important.

- Increased responsibility for enterprise risk management (ERM).

- Diversity, equity and inclusion (DE&I) reporting will be more of a competitive differentiator.

- Automation will accelerate.

- There will be greater demand for upskilling and continued education for professionals.

Ultimately, today’s accountants need to be multidisciplinary. It’s vital to have a breadth of knowledge—aim to be ‘key-shaped’ employees with varied skills, that’s the value companies are looking for.

If you’re keen to find out more, you can check out IMA’s Management Accounting Competency Framework to assess your own skills, and find out the critical skills you need as an accountant or finance professional.

4. Pricing your services: How to review your strategy

Most customers assume that the higher the price, the better the quality. But is that really true? Eduard Ortega, CPA, CMA at Remotely Philippines, shared some key tips on how to review your current strategy.

Your pricing strategy is ultimately dependent on your objectives—you can be pricing a premium if you want your firm to come across as offering quality services versus affordable services. If you’re value-adding to your services, you should also increase your prices.

It also depends on your buyers—who are you selling your services to? What are they looking for? Demand and supply also affects your pricing strategy. Is there an increase in demand? Like during the pandemic where there was a surge in businesses looking for advisory services?

Local laws and regulations can also affect your pricing strategy due to legislative restrictions—you might not be able to have as much flexibility with your pricing due to a certain ceiling.

What’s the significance of a proper pricing strategy?

- It influences customer or client perception—price is the determinant of value and quality. It increases your customer/client loyalty, as well as brand recognition.

- It helps with competitor analysis—your pricing strategy affects your market share, and provides a competitive advantage against your main competitors.

- It increases revenue and profitability—by pricing your services properly, you help to drive growth for your business by maximising profits.

There are both internal and external considerations you should have in pricing your services, such as:

- Internal factors: Costs, objectives, organisational factors, marketing mix, service differentiation.

- External factors: Suppliers, buyers, demand, economic conditions, government, competition.

When you should you review your prices?

You should review your prices regularly and more often than you have previously, due to the constantly changing conditions. The market you operate in and the services you offer will dictate how often prices should be reviewed.

Different pricing strategies

New service pricing strategies

- Price skimming—if you’re introducing a new service, it means you can start your pricing high. As more competitors join the industry, prices will be forced to go down in order to compete.

- Pricing for market penetration—if you’re trying to break into the market with your service, you have to price your product or service competitively in order to win some market share.

Price adjustment strategies

- Pricing at a premium—customers need to perceive the product/service as being worthy of the higher price tag.

- Economy pricing–effective for large companies, which aims to attract the most price-conscious consumers.

- Psychology pricing—using marketing techniques to encourage customers to respond emotionally.

- Segmented pricing—selling a product or service at two or more prices (like movie tickets for example).

- Discounts and allowances—these may include volume purchases, early clearance of bills, off season purchases or stays etc.

- Promotional pricing—the reduction of product or service prices below the market price or even below cost for a temporary period of time.

- Geographical pricing—adjusting the list price of the products based on the location of the consumer.

- Dynamic pricing—adjusting the price of products continuously to meet the needs of individual customers (like airplane tickets for example).

Ultimately, you decide which pricing strategy works best for your industry and business—don’t forget to review it regularly and use these strategies along the way!

5. How can tech help you create a win-win relationship with clients?

Chee Siew Fai, an audit partner at FOZL Assurance, shared some valuable tips. As an accountant, you are more than a number cruncher for a business. Clients approach you to get help on how they can run their business better with expert financial advice. Merely processing numbers and generating reports will not be enough to satisfy your clients—to deepen the relationship, you must provide more value for clients.

Chee Siew Fai, an audit partner at FOZL Assurance, shared some valuable tips. As an accountant, you are more than a number cruncher for a business. Clients approach you to get help on how they can run their business better with expert financial advice. Merely processing numbers and generating reports will not be enough to satisfy your clients—to deepen the relationship, you must provide more value for clients.

And how can you value-add? By utilising technology. With a wide array of tools available in the market now, you can use them to analyse client data quickly. Your processes become quicker and more efficient, increasing the amount of work and the number of clients your firm can handle. Operations are less error-prone, and your services provided are of a higher value. This improves both productivity and profitability, and it’s a win-win solution for both you and your client, as well as the bottom line.

Using technology to boost productivity (doing more with less)

Automating many of the repetitive manual processes accountants do every day helps to create a much more efficient practice. Introducing new software systems to accounting firms can involve a bit of hand-holding, but ultimately most see the benefits of having automated systems carry out the most time-consuming administrative tasks. By making technology do as much as possible, your firm can free up precious time to focus on more strategic parts of the business.

Using technology to improve client communication

Working in the cloud speeds up the communication and processes of bookkeeping and accounting records. Key numbers are much more easily accessible from anywhere and at anytime, making it easier for both the client and accountant to answer any queries or flag issues.

Technology has revolutionised communication in the accounting profession—you now have access to various tools and platforms that make communication faster and more efficient. Email and video conferencing enables you to streamline your work, collaborate more effectively, and meet deadlines. However, there are also challenges such as data security and the potential for miscommunication using digital channels. But with proper training and education, technology can become a powerful solution for everyone to utilise.

Using technology to deepen client relationships

With the time saved from automating processes, you have more time to focus on building and strengthening client relationships. By getting to know them better on a deeper level, you can offer value-added services easily, use smart reporting tools to enhance your analysis of your client’s numbers, and improve forecasting. This provides them with more insightful advice and support, and in turn helps to deepen their trust in your expertise.

The impact of technology on accounting has seen a change in the processes involved. Technology cannot fully replace accounting expertise—but rather, it helps accountants do what they do best while leaving repetitive, mundane tasks to technology. It offers more value for both the accountant and their clients.

Maintaining healthy, long-term relationships with your clients are essential to the firm’s success. When you understand their needs and requirements better, you can address their concerns more effectively in a timely manner, and this eventually leads to enhanced customer loyalty.

As you create meaningful wins for your clients, it generates growth for their business, and this in turn benefits you too with positive reviews and referrals. It’s a win-win situation!

The wrap up

There’s been so much chatter about digital transformation and the importance of technology in the accounting and finance sector. But one thing is clear—focus on problem solving, make the most of your tech stack, and keep reviewing, improving and evolving.

Thank you for reading till the end, and we hope that these insights have been of use to you in some way or another. That’s a wrap — we look forward to seeing you at our next event!

Check out our State of Payroll and Technology Report for more valuable insights. We surveyed practitioners in Singapore and Malaysia about their accounting and payroll services, and attitudes towards technology. Our key findings revealed that future-focused processes will help build successful practices that the evolving industry demands, and support a revenue-driving payroll function.

Related Resources

-

Read more: Product Update: January 2026

Read more: Product Update: January 2026Product Update: January 2026

Welcome to the January 2026 product update from the Employment Hero team. We’ve got lots to share around Custom Forms,…

-

Read more: Product Update: December 2025

Read more: Product Update: December 2025Product Update: December 2025

Welcome to the December 2025 product update from the Employment Hero team. We’ve got lots to share around Custom Forms,…

-

Read more: Product Update: November 2025

Read more: Product Update: November 2025Product Update: November 2025

Welcome to the November 2025 product update from the Employment Hero team. We’ve got lots to share around Workflows, Rostering,…